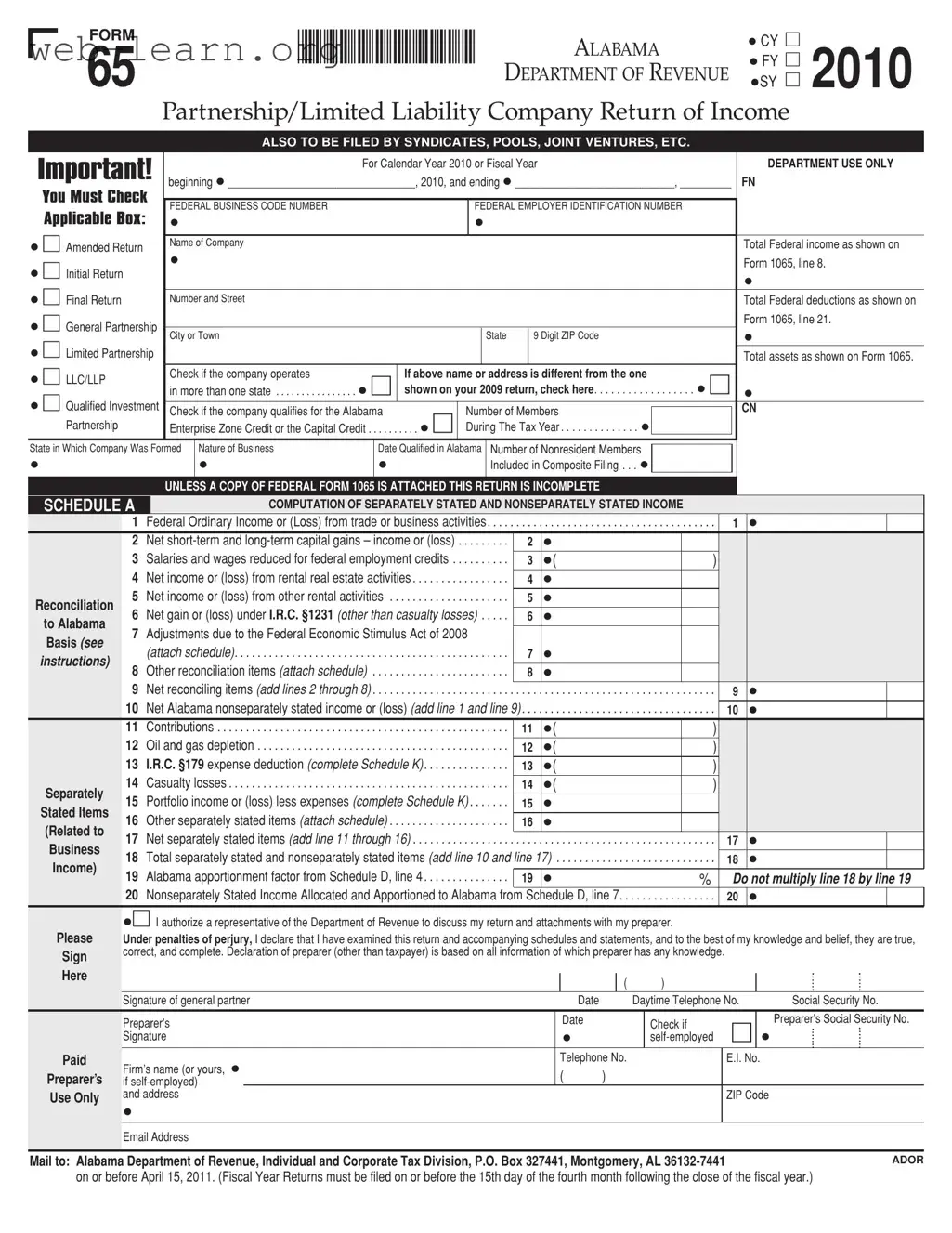

The Alabama 65 form serves as a crucial document for partnerships and limited liability companies operating within the state, facilitating the accurate reporting of income and deductions for tax purposes. This form is required not only from general partnerships and limited partnerships but also from syndicates, pools, joint ventures, and other similar entities. For the calendar year 2010 or any designated fiscal year, the form captures essential financial data, including total federal income, deductions, and assets, as reported on federal Form 1065. Furthermore, it requires the identification of the company’s business nature, its operational states, and the number of nonresident members. The form also includes various schedules that guide users in calculating separately stated and non-separately stated income, ensuring compliance with Alabama tax regulations. Notably, it mandates the attachment of federal Form 1065, without which the return is deemed incomplete. The Alabama 65 form is not merely a tax obligation; it reflects the financial health and operational scope of the business, making it vital for both compliance and strategic financial planning.

| Fact Name | Description |

|---|---|

| Form Purpose | The Alabama 65 form is used for the Partnership/Limited Liability Company Return of Income. |

| Filing Requirement | This form must also be filed by syndicates, pools, joint ventures, and similar entities. |

| Tax Year | The form is specifically for the calendar year 2010 or the fiscal year beginning in 2010. |

| Governing Law | The Alabama 65 form is governed by Alabama Code § 40-14-1 and related tax regulations. |

| Federal Attachments | A copy of Federal Form 1065 must be attached; otherwise, the return is considered incomplete. |

| Income Reporting | Entities must report total federal income, deductions, and assets as shown on Form 1065. |

| Composite Filing | Nonresident members included in composite filing must be reported on the form. |

| Signature Requirement | The form must be signed by a general partner, declaring the accuracy of the information provided. |

| Filing Deadline | Returns are due on or before April 15, 2011, for calendar year filers. |

| Mailing Address | Completed forms should be mailed to the Alabama Department of Revenue, Individual and Corporate Tax Division. |

The Alabama 65 form is essential for partnerships and limited liability companies to report their income and deductions for a specific tax year. Completing this form accurately is crucial for compliance with state tax regulations. Below are the steps to fill out the form properly.

After completing the form, it is essential to submit it to the Alabama Department of Revenue by the specified deadline. Ensure all attachments are included to avoid any delays or issues with processing your return.

The Alabama 65 form is a tax return specifically designed for partnerships, limited liability companies (LLCs), and other similar entities operating in Alabama. It is used to report income, deductions, and various tax-related information for the calendar year or fiscal year as specified by the entity.

Any partnership, limited liability company, syndicate, pool, or joint venture that conducts business in Alabama must file the Alabama 65 form. This includes entities that may operate in multiple states but have income that is subject to Alabama taxation.

The form requires detailed information, including:

The Alabama 65 form must be filed by April 15 of the following year for calendar year filers. For fiscal year filers, the return is due on the 15th day of the fourth month following the close of the fiscal year.

Filing the Alabama 65 form late may result in penalties and interest on any unpaid tax. It is essential to file on time to avoid these additional charges. If there are extenuating circumstances, it may be beneficial to consult with a tax professional for guidance.

Yes, the Alabama 65 form can be amended if errors are discovered after the initial filing. An amended return should be marked clearly as an amended return, and it is crucial to provide accurate information to correct any discrepancies.

To ensure the return is complete, it is necessary to attach a copy of the federal Form 1065. Additionally, any schedules or documents that support the income and deductions claimed should also be included.

Yes, nonbusiness income must be reported separately on Schedule B of the Alabama 65 form. It is essential to identify and categorize all nonbusiness income, loss, and related expenses accurately.

If you need help with the Alabama 65 form, it is advisable to contact a tax professional or the Alabama Department of Revenue. They can provide guidance and answer specific questions related to your situation.

Filling out the Alabama 65 form can be a complex process, and many individuals make mistakes that could lead to delays or issues with their tax returns. One common error is failing to check the appropriate box at the top of the form. Whether it’s an initial, amended, or final return, marking the correct option is crucial. Neglecting this step can result in confusion and potentially cause the return to be processed incorrectly.

Another frequent mistake involves not providing complete and accurate information about the company. This includes the company name, address, and federal employer identification number (FEIN). If any of these details are incorrect or missing, it can lead to complications in processing the return. Always double-check this information to ensure it matches what is on file with the IRS.

Many people also overlook the requirement to attach a copy of the federal Form 1065. The Alabama Department of Revenue specifies that without this attachment, the return is considered incomplete. This oversight can lead to unnecessary delays or even penalties. It’s essential to ensure that all required documents are included before submission.

Another common error is in the computation of income and deductions. When transferring figures from Form 1065 to the Alabama 65 form, individuals sometimes miscalculate or misplace numbers. This can result in incorrect tax liabilities. It is advisable to take time to verify all calculations and ensure they are accurately reflected on the form.

Additionally, some filers forget to account for nonresident members. If a partnership includes members who do not reside in Alabama, it is important to indicate this on the form. Failing to do so can lead to incorrect apportionment of income and potential issues with tax compliance.

Another mistake involves not providing sufficient detail in the schedules attached to the form. For instance, Schedule B requires a breakdown of nonbusiness income, loss, and expenses. Incomplete information here can lead to misunderstandings about the nature of the income being reported. It is vital to provide a clear and detailed account of all relevant figures.

Many individuals also fail to sign the form. The signature is a legal declaration that the information provided is true and accurate. Without it, the return may be deemed invalid. Ensure that the appropriate parties sign the form before submission to avoid this common pitfall.

Lastly, individuals sometimes miss the deadline for filing the Alabama 65 form. It is important to be aware of the due date, which can vary based on whether the entity operates on a calendar year or a fiscal year. Late submissions can incur penalties, so keeping track of deadlines is essential for compliance.

The Alabama 65 form is essential for partnerships and limited liability companies to report their income to the state. It is important to complete this form accurately and attach the necessary documents to ensure compliance with state regulations. Below is a list of other forms and documents often used alongside the Alabama 65 form.

Ensure that all relevant forms are completed and submitted along with the Alabama 65 form to avoid any delays or issues with your tax filings. Each document plays a critical role in providing a comprehensive overview of the partnership's financial activities and compliance with state laws.

When filling out the Alabama 65 form, it’s important to follow specific guidelines to ensure everything is accurate and complete. Here’s a list of what you should and shouldn’t do:

Misconception 1: The Alabama 65 form is only for partnerships.

This form is not limited to partnerships. It also applies to limited liability companies (LLCs), syndicates, pools, joint ventures, and other similar entities.

Misconception 2: Filing the Alabama 65 form is optional.

Filing the Alabama 65 form is mandatory for entities that meet the criteria outlined by the Alabama Department of Revenue. Failure to file can result in penalties.

Misconception 3: The Alabama 65 form can be submitted without attachments.

It is essential to attach a copy of Federal Form 1065. Without this attachment, the return is considered incomplete.

Misconception 4: Only income needs to be reported on the form.

Both income and deductions must be reported. The form requires detailed information on total federal income, deductions, and assets.

Misconception 5: The Alabama 65 form does not require specific accounting methods.

The form requires the filer to indicate their method of accounting, whether cash, accrual, or another method. This is crucial for accurate reporting.

Misconception 6: Filing deadlines for the Alabama 65 form are flexible.

There are strict deadlines for filing. The form must be submitted by April 15 for calendar year returns or by the 15th day of the fourth month following the close of the fiscal year.

The Alabama 65 form is used for filing income tax returns for partnerships and limited liability companies (LLCs) in Alabama.

This form must be filed for the calendar year or fiscal year as specified, ensuring that the correct dates are entered in the designated fields.

It is essential to check the appropriate box to indicate whether the return is an initial, amended, or final return.

All federal income and deductions must be accurately reported, specifically referencing Form 1065 for total federal income and deductions.

If the company operates in more than one state, it is necessary to check the corresponding box on the form.

Inclusion of a copy of Federal Form 1065 is mandatory; failure to attach this document renders the return incomplete.

Schedule A must be completed to compute separately stated and non-separately stated income, with careful attention to each line item.

Taxpayers must sign the form, declaring that the information provided is true and complete, under penalties of perjury.

The completed form should be mailed to the Alabama Department of Revenue by the specified deadline to avoid penalties.