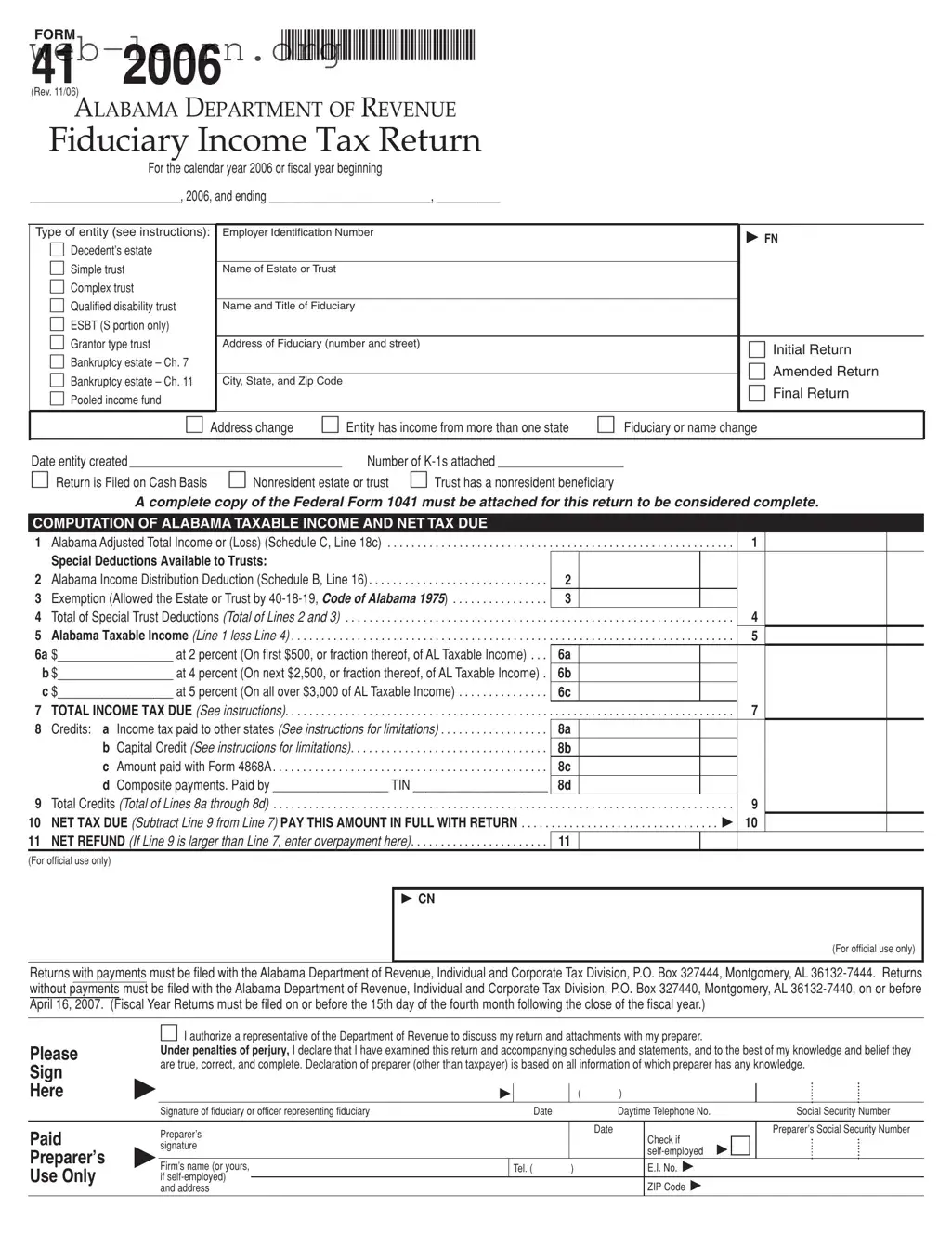

The Alabama 41 form is a crucial document for fiduciaries managing estates and trusts in Alabama. Designed for the reporting of income tax, this form must be accurately completed for the calendar year 2006 or for fiscal years beginning in that year. Various entities, including decedent’s estates, simple trusts, and complex trusts, utilize this form to report their income, deductions, and tax liabilities. The Alabama Department of Revenue requires a complete copy of the Federal Form 1041 to accompany the Alabama 41 form for it to be deemed complete. This form not only captures essential information such as the employer identification number, the name and title of the fiduciary, and the address of the fiduciary, but it also includes critical sections for calculating Alabama taxable income and net tax due. Special deductions available to trusts and the computation of Alabama income distribution deductions are also integral parts of this form. Moreover, changes in Alabama tax law, particularly those affecting estates and trusts, have made it imperative for fiduciaries to stay informed and compliant. Timely submission of the Alabama 41 form is essential to avoid penalties, and understanding its requirements can significantly ease the process of fulfilling fiduciary responsibilities.

| Fact Name | Description |

|---|---|

| Form Purpose | The Alabama 41 form is used for filing the Fiduciary Income Tax Return for estates and trusts. |

| Governing Law | This form is governed by the Code of Alabama 1975, specifically §40-18-25(b) and §40-18-19. |

| Filing Deadline | Returns must be filed by April 16, 2007, for calendar year entities, or by the 15th day of the fourth month following the close of the fiscal year. |

| Entity Types | Entities that can file include decedent's estates, simple trusts, complex trusts, and bankruptcy estates, among others. |

| K-1 Attachments | Taxpayers must attach a complete copy of the Federal Form 1041 for the return to be considered complete. |

| Income Sources | The form accounts for income from various sources, including business income, dividends, and capital gains. |

| Tax Rates | Alabama tax rates for fiduciary income range from 2% to 5%, depending on the taxable income amount. |

| Special Deductions | Trusts can claim special deductions, including the Alabama Income Distribution Deduction and exemptions allowed by law. |

| Charitable Contributions | There is a specific schedule for reporting Alabama charitable deductions, applicable to certain types of trusts. |

| Changes in Law | The Subchapter J and Business Trust Conformity Act was enacted in 2006, impacting how estates and trusts are taxed retroactively from 2005. |

Filling out the Alabama 41 form is a straightforward process that requires careful attention to detail. This form is essential for reporting fiduciary income tax for estates and trusts. Make sure to have all necessary documentation ready, including the Federal Form 1041, as it must be attached for the return to be complete.

After completing the form, ensure that all required attachments, including a copy of the Federal Form 1041, are included. Submit the return to the appropriate address based on whether you are making a payment or not. Keep a copy of the completed form for your records.

The Alabama 41 form is the Fiduciary Income Tax Return used for reporting the income of estates and trusts in Alabama. It is required for the calendar year 2006 or for fiscal years beginning in 2006. This form is essential for fiduciaries to report the income, deductions, and tax liability of the estate or trust.

The form must be filed by fiduciaries of decedent's estates, simple trusts, complex trusts, qualified disability trusts, bankruptcy estates, and pooled income funds. If the entity has income from more than one state or has a nonresident beneficiary, the Alabama 41 form is also necessary.

To complete the Alabama 41 form, you will need:

The form must be filed by April 16, 2007, for calendar year returns. For fiscal year returns, the deadline is the 15th day of the fourth month following the close of the fiscal year. Timely filing is crucial to avoid penalties.

If you need to amend your return, you should check the box indicating it is an amended return on the form. Ensure that all corrections are clearly noted, and submit the amended return to the appropriate address provided for returns without payments.

Yes, trusts may qualify for special deductions such as the Alabama Income Distribution Deduction and an exemption allowed by Alabama law. The form includes specific lines to calculate these deductions, which can help reduce the taxable income of the estate or trust.

A complete copy of the Federal Form 1041 must be attached for the Alabama 41 form to be considered complete. This federal form provides detailed information about the income, deductions, and distributions of the estate or trust, which is crucial for accurate state tax calculations.

If the estate or trust has a nonresident beneficiary, it is important to indicate this on the Alabama 41 form. Additionally, ensure that you follow the specific instructions related to nonresident beneficiaries to accurately report their income and any applicable deductions.

Completed returns with payments should be sent to the Alabama Department of Revenue, Individual and Corporate Tax Division, P.O. Box 327444, Montgomery, AL 36132-7444. Returns without payments should be sent to P.O. Box 327440, Montgomery, AL 36132-7440.

If you have questions while completing the Alabama 41 form, it is advisable to consult the instructions provided with the form. For additional assistance, you may contact the Alabama Department of Revenue directly or seek guidance from a tax professional.

When filling out the Alabama 41 form, individuals often make several common mistakes that can lead to delays or complications in processing their returns. One significant error occurs when the Employer Identification Number (EIN) is either omitted or incorrectly entered. This number is crucial for identifying the estate or trust. If the EIN is wrong, the Alabama Department of Revenue may not be able to match the return with the correct entity, resulting in potential penalties or further inquiries.

Another frequent mistake involves failing to attach a complete copy of the Federal Form 1041. This form is essential for the Alabama return to be considered complete. Without it, the state may reject the submission or request additional information, prolonging the process unnecessarily. It is vital to ensure that all required documents accompany the Alabama 41 form.

Additionally, many individuals overlook the importance of accurately reporting the Alabama Taxable Income. Errors in calculating the income or deductions can lead to incorrect tax amounts due. For instance, miscalculating the Alabama Adjusted Total Income or incorrectly entering the Alabama Income Distribution Deduction can significantly impact the total tax liability. It is advisable to double-check all calculations to ensure accuracy.

Lastly, some filers neglect to sign the form or provide the necessary contact information. The signature of the fiduciary or officer representing the fiduciary is required for the return to be valid. Additionally, including a daytime telephone number can facilitate communication should any questions arise during processing. Ensuring that all sections of the form are completed accurately and thoroughly can help prevent unnecessary complications.

The Alabama 41 form is essential for fiduciaries managing estates or trusts in Alabama. It provides a structured way to report income and calculate taxes owed. Alongside this form, several other documents may be required to ensure compliance with state tax laws. Below is a list of forms and documents that are often used in conjunction with the Alabama 41 form.

Filing the Alabama 41 form and its accompanying documents is a critical step for fiduciaries. Understanding the purpose of each form can help ensure compliance and minimize potential tax liabilities. It is advisable to consult with a tax professional to navigate these requirements effectively.

When filling out the Alabama 41 form, attention to detail is crucial. Here are some important dos and don'ts to ensure a smooth filing process.

By following these guidelines, individuals can navigate the complexities of the Alabama 41 form more effectively.

Understanding the Alabama 41 form can be crucial for fiduciaries managing estates and trusts. However, several misconceptions often arise. Here are six common misunderstandings:

This form is applicable to various types of entities, including decedent's estates, simple trusts, and even bankruptcy estates. It is not limited to complex trusts.

Even if there is no income, filing may still be required. It is important to check the specific circumstances and requirements for the entity.

A complete copy of the Federal Form 1041 must be attached for the Alabama 41 form to be considered complete. This is a necessary step for accurate processing.

There are strict deadlines for filing the Alabama 41 form. Returns must be submitted by April 16, 2007, for the calendar year 2006, or within four months after the close of the fiscal year for fiscal returns.

Documentation is essential. Each deduction claimed must be supported by appropriate records and calculations as outlined in the instructions.

The Alabama Department of Revenue regularly updates information regarding tax laws and regulations. It is beneficial to check their website for the latest guidance and updates.

Here are some key takeaways about filling out and using the Alabama 41 form: