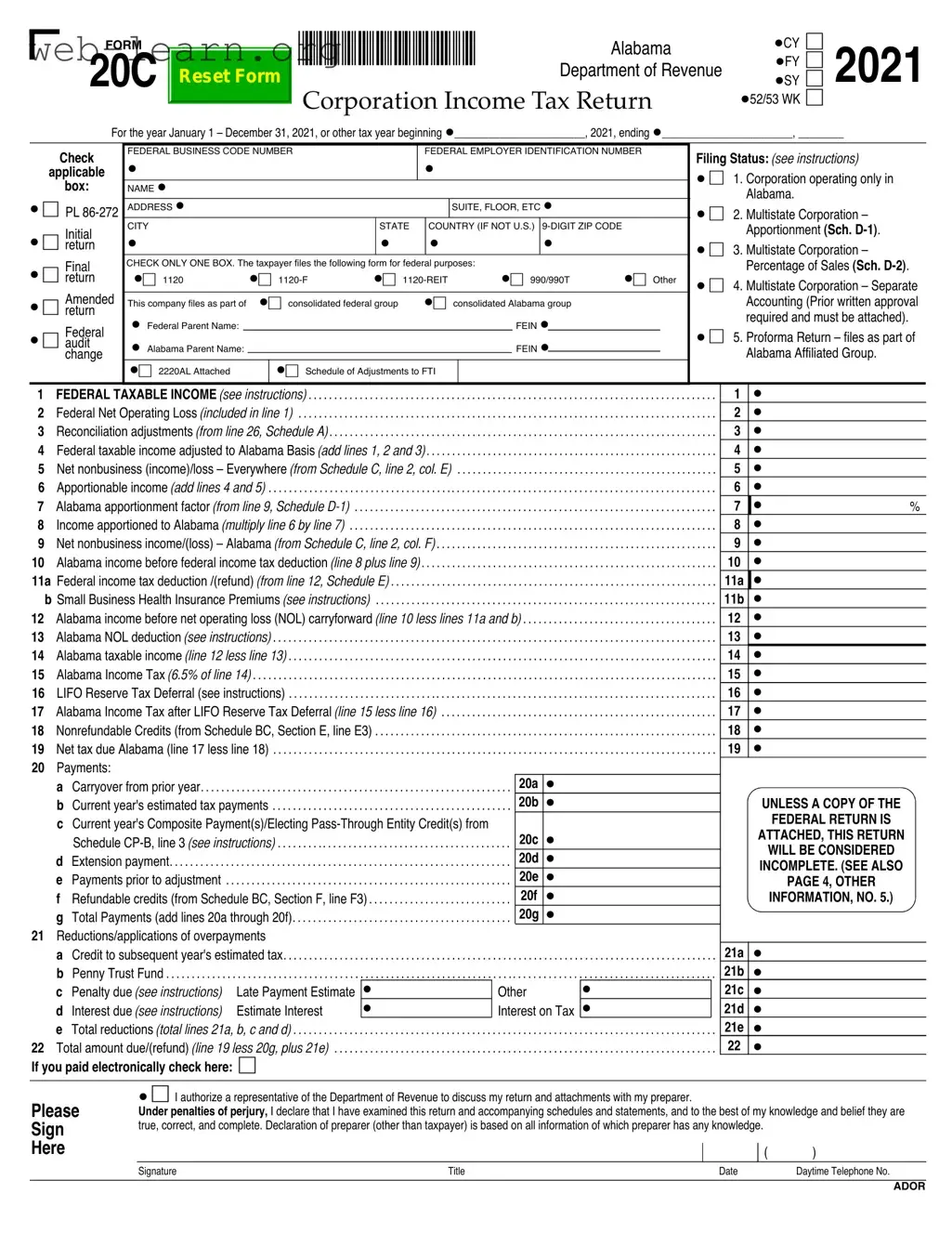

The Alabama 20C form is a crucial document for corporations operating within the state, serving as the Corporation Income Tax Return. It is designed to capture essential financial information for the tax year, which can run from January 1 to December 31, or another specified tax year. This form requires corporations to disclose their federal business code number and employer identification number, along with their filing status, which may indicate whether they operate solely in Alabama or across multiple states. Key sections of the form include reporting federal taxable income, adjustments for net operating losses, and reconciliation of federal income to Alabama taxable income. Corporations must also provide details about their apportionable income, which determines how much of their income is taxable in Alabama versus other states. The form includes various schedules, such as Schedule A for reconciliation adjustments and Schedule D-1 for apportionment factors, ensuring that all income is accurately accounted for. Completing the Alabama 20C form correctly is essential for compliance with state tax laws and for determining the corporation's tax liability, which is calculated at a rate of 6.5% on taxable income. Understanding the intricacies of this form is vital for corporations to navigate their tax obligations effectively.

| Fact Name | Detail |

|---|---|

| Form Purpose | The Alabama 20C form is used for filing the Corporation Income Tax Return for corporations operating in Alabama. |

| Tax Year | This form is applicable for the tax year beginning January 1 and ending December 31, 2010, or for other specified tax years. |

| Filing Status Options | Corporations can select from various filing statuses, including single-state, multistate initial, final, separate, and amended returns. |

| Federal Business Code | Corporations must provide their Federal Business Code Number and Federal Employer Identification Number (FEIN) on the form. |

| Alabama Apportionment Factor | The form includes a section to calculate the Alabama apportionment factor, which determines how much income is taxable in Alabama. |

| Governing Law | The Alabama 20C form is governed by §40-18-33 of the Code of Alabama 1975, which outlines the definition of Alabama Taxable Income. |

| Net Operating Loss (NOL) | Corporations can calculate and carry forward their Alabama Net Operating Loss, as detailed in Schedule B of the form. |

| Credits and Deductions | The form allows for various credits and deductions, including the federal income tax deduction and specific Alabama tax credits. |

| Submission Requirements | A complete return must include all required schedules and attachments; otherwise, it may be deemed incomplete by the Alabama Department of Revenue. |

Completing the Alabama 20C form involves several steps to ensure accurate reporting of corporate income. Gather all necessary financial documents and information before starting. This will help streamline the process and minimize errors.

The Alabama 20C form is the Corporation Income Tax Return specifically designed for corporations operating in Alabama. It is used to report income, calculate tax liability, and determine any applicable credits or deductions for the tax year. This form must be filed by corporations that are either solely based in Alabama or operate across multiple states.

Any corporation that is doing business in Alabama must file the Alabama 20C form. This includes corporations that are incorporated in Alabama as well as those that are incorporated elsewhere but have a business presence in the state. Additionally, corporations that are part of a consolidated federal return must also file this form, indicating their status accordingly.

The deadline for filing the Alabama 20C form is typically the 15th day of the 4th month following the end of the corporation’s tax year. For most corporations with a calendar year ending December 31, the due date would be April 15 of the following year. If the due date falls on a weekend or holiday, the deadline is extended to the next business day.

To complete the Alabama 20C form, corporations must provide various details, including:

The Alabama income tax is calculated at a rate of 6.5% on the corporation's taxable income after making necessary adjustments for Alabama tax purposes. The form includes specific lines to report federal taxable income, adjustments, and any nonbusiness income or losses that affect the taxable amount. Corporations must carefully follow the instructions to ensure accurate calculations.

If a corporation cannot meet the filing deadline, it may request an automatic extension. This can typically be done by filing Form 20C with the appropriate payment of estimated taxes owed. However, it is important to note that an extension to file is not an extension to pay any taxes due. Late payments may incur penalties and interest.

The completed Alabama 20C form should be mailed to the Alabama Department of Revenue at the designated address for corporate tax returns. For most corporations, this is:

Individual and Corporate Tax Division

Corporate Tax Section

PO Box 327435

Montgomery, AL 36132-7435

Corporations should ensure that they include any required attachments, such as copies of federal returns, to avoid delays or issues with processing.

Filling out the Alabama 20C form can be a complex process, and mistakes can lead to delays or complications. One common error is failing to provide the correct Federal Employer Identification Number (FEIN). This number is crucial for identification and should match what the IRS has on file. Double-check this number to avoid potential issues.

Another frequent mistake involves selecting the wrong filing status. The form includes multiple options, such as "Initial," "Final," or "Amended." Selecting the incorrect status can result in the return being processed incorrectly. Ensure that the chosen status accurately reflects the corporation's situation for the tax year.

People often forget to include the state of incorporation and the date of incorporation. These details are essential for establishing jurisdiction and should be filled in clearly. Leaving this information blank can lead to processing delays or further inquiries from the Alabama Department of Revenue.

Another common oversight is neglecting to complete the apportionment factor section accurately. This section requires specific calculations based on business operations in Alabama versus other states. Errors here can affect tax liabilities significantly, so it’s crucial to follow the instructions carefully.

Additionally, failing to attach necessary documentation, such as the federal return, can result in the return being deemed incomplete. The form clearly states that without these attachments, the return may not be accepted. Make sure all required documents are included before submission.

Some filers also miscalculate their Alabama taxable income. This mistake often stems from incorrect additions or deductions. It’s vital to review each line carefully to ensure accuracy in calculations, as this can directly impact the tax owed or refund expected.

Another error involves the signature section. The form must be signed by an authorized representative. Incomplete or missing signatures can lead to delays in processing. Always ensure that the signature is present and that the title of the signer is included.

Lastly, many people overlook the contact information for inquiries. Providing a clear point of contact can facilitate communication with the Alabama Department of Revenue should any questions arise. Ensure that this section is filled out completely to avoid unnecessary delays.

The Alabama 20C form is a crucial document for corporations filing their income tax returns in Alabama. However, several other forms and documents are often required to accompany it, ensuring compliance with state tax regulations. Below is a list of these forms, each serving a specific purpose in the overall tax filing process.

Each of these documents plays a vital role in ensuring that corporations meet their tax obligations accurately and efficiently. Proper completion and submission of these forms alongside the Alabama 20C form can help avoid potential issues with the Alabama Department of Revenue.

The Alabama 20C form, which is used for corporate income tax returns, shares similarities with several other tax-related documents. Each of these forms serves a unique purpose but often contains overlapping information regarding income, deductions, and tax calculations. Below is a list of nine documents that are similar to the Alabama 20C form, along with a brief explanation of how they are alike:

When filling out the Alabama 20C form, there are several important dos and don'ts to keep in mind. Here’s a helpful list to guide you through the process:

By following these guidelines, you can navigate the Alabama 20C form with confidence and ease.

Misconception 1: The Alabama 20C form is only for corporations operating solely in Alabama.

In reality, the form is designed for both single-state and multistate corporations. Multistate corporations must complete additional sections to account for income apportionment across different states.

Misconception 2: Filing the Alabama 20C form guarantees a tax refund.

Filing does not automatically result in a refund. The outcome depends on various factors, including the corporation's taxable income and any applicable deductions or credits.

Misconception 3: The Alabama 20C form is the same as the federal corporate tax return.

While there are similarities, the Alabama 20C form has specific requirements and calculations unique to Alabama tax law. Corporations must adjust their federal taxable income to align with Alabama's tax regulations.

Misconception 4: All deductions available on the federal return apply to the Alabama 20C form.

This is not true. Certain deductions allowed federally may not be applicable at the state level. Corporations must review Alabama's specific tax laws to determine which deductions they can claim.

Misconception 5: Filing an amended return is unnecessary if no changes were made to the federal return.

Even if the federal return remains unchanged, corporations may still need to amend their Alabama return if they discover errors or if there are changes in state-specific tax laws that affect their taxable income.

The Alabama 20C form is specifically designed for corporations operating within Alabama or those with multistate operations. Ensure that the correct filing status is selected based on your corporation's operations.

Accurate reporting of federal taxable income is crucial. Lines 1 through 14 require detailed calculations to adjust federal income to reflect Alabama taxable income, including any net operating losses and apportionable income.

Documentation is essential. A copy of the federal return must accompany the Alabama 20C form to avoid the return being considered incomplete. This includes all necessary schedules and supporting documentation.

Be mindful of deadlines. The form must be filed by the due date to avoid penalties and interest. Extensions may be available, but they require timely submission of the appropriate forms.