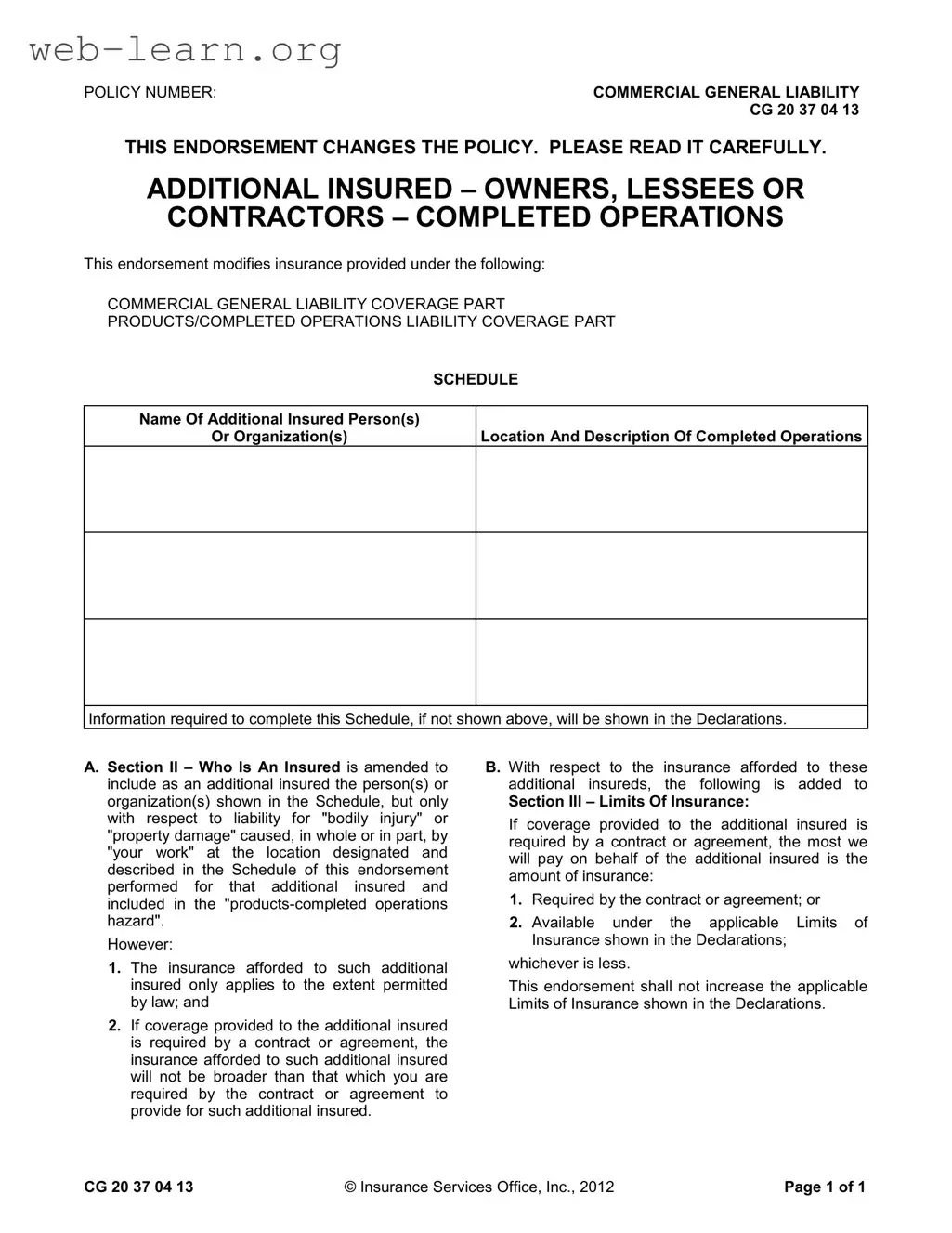

The Additional Insured form, specifically the Commercial General Liability CG 20 37 04 13 endorsement, plays a crucial role in defining the coverage landscape for businesses and contractors. This endorsement modifies the existing insurance policy, extending coverage to additional parties, typically owners, lessees, or contractors, for completed operations. It is essential to understand that this form includes specific details such as the names of additional insured persons or organizations and the location and description of the completed operations. The form clearly outlines that the insurance applies to liability for bodily injury or property damage arising from the work performed for these additional insured parties, but only to the extent permitted by law. Importantly, if the coverage is mandated by a contract, the insurance provided will not exceed the limits required by that contract or the amounts available under the policy's declarations. This ensures that while additional insureds receive necessary protection, the coverage remains aligned with the contractual obligations of the primary insured. Understanding these nuances can help businesses navigate their insurance needs effectively.

| Fact Name | Description | Governing Law |

|---|---|---|

| Policy Number | This endorsement is identified by the policy number CG 20 37 04 13. | Varies by state |

| Coverage Type | The endorsement modifies coverage under the Commercial General Liability policy. | Varies by state |

| Additional Insured | It includes owners, lessees, or contractors as additional insureds. | Varies by state |

| Scope of Coverage | Coverage is limited to liability for bodily injury or property damage caused by the insured's work. | Varies by state |

| Location Requirement | The endorsement specifies the location and description of completed operations. | Varies by state |

| Contractual Limitations | If required by contract, the coverage cannot exceed what is stipulated in that contract. | Varies by state |

| Limits of Insurance | The maximum amount payable is the lesser of the contract limit or the policy limit. | Varies by state |

| Modification of Insured | Section II of the policy is amended to include additional insureds. | Varies by state |

| Insurance Services Office | This endorsement is published by the Insurance Services Office, Inc. | Varies by state |

| Effective Date | The form was issued on April 13, 2013. | Varies by state |

Filling out the Additional Insured form is a straightforward process that requires attention to detail. This form is essential for ensuring that specific individuals or organizations are covered under your insurance policy for certain liabilities. Follow the steps below to complete the form accurately.

Once you have filled out and submitted the form, your insurance provider will process it. They may reach out if they need any additional information or clarification. It’s always a good idea to follow up to ensure everything is in order.

What is the purpose of the Additional Insured form?

The Additional Insured form is designed to extend liability coverage to other parties, such as owners, lessees, or contractors, who may be held responsible for injuries or damages related to your work. This endorsement ensures that these additional insured parties are protected under your Commercial General Liability policy, specifically for completed operations.

Who qualifies as an additional insured?

Individuals or organizations listed in the Schedule of the endorsement qualify as additional insureds. This typically includes clients, project owners, or contractors that you are working for. Their coverage is limited to liability arising from your work, specifically at the location described in the endorsement.

What types of incidents are covered under the Additional Insured endorsement?

The endorsement covers liability for "bodily injury" or "property damage" that occurs as a result of your work. This includes incidents that happen during the completed operations phase of a project. However, the coverage is only valid to the extent permitted by law and is subject to the specific terms of your contract with the additional insured.

Are there any limitations to the coverage provided?

Yes, there are limitations. The coverage provided to the additional insured cannot exceed what is required by your contract with them. Additionally, it will not be broader than the coverage you are obligated to provide. This means that if your contract specifies a certain level of coverage, that will be the maximum available to the additional insured.

How does the limit of insurance work for additional insureds?

The limit of insurance for additional insureds is determined by the lesser of two amounts: the coverage required by the contract or the limits available under your policy. This means that if your policy has a cap on coverage, the additional insured will only receive the amount specified in the contract or the policy limit, whichever is lower.

Can the Additional Insured endorsement increase my policy limits?

No, the endorsement does not increase the overall limits of your insurance policy. The limits of insurance stated in the Declarations remain unchanged. Therefore, it is essential to ensure that your policy limits are adequate to cover both your needs and those of any additional insured parties.

How should I complete the Additional Insured form?

To complete the form, you need to provide the names of the additional insured individuals or organizations and a description of the completed operations. If this information is not included in the form itself, it will typically be found in the Declarations of your policy. Ensure that all details are accurate to avoid any coverage issues in the future.

When filling out the Additional Insured form, individuals often make several common mistakes that can lead to complications later on. One frequent error is failing to accurately identify the name of the additional insured. It is crucial to ensure that the name matches exactly with the legal entity or person to avoid any issues with coverage.

Another mistake is not providing a clear description of the completed operations. This section should detail the specific work being done for the additional insured. Vague descriptions can lead to misunderstandings about what is covered, potentially leaving parties exposed to liability.

Some people neglect to check the policy number and ensure it corresponds with the correct coverage. This oversight can result in the additional insured not being properly covered under the intended policy, which may cause significant problems if a claim arises.

In addition, individuals sometimes overlook the importance of understanding the limits of insurance specified in the form. It is essential to note that the coverage provided to the additional insured cannot exceed what is stipulated in the contract or agreement. Misinterpreting this can lead to inadequate protection.

Lastly, failing to consider the legal requirements for additional insured status can create issues. The insurance provided must comply with applicable laws, and not adhering to these can result in gaps in coverage. Each of these mistakes can have serious implications, so careful attention to detail is necessary when completing the form.

The Additional Insured form is a crucial document in the realm of liability insurance. However, it often works in tandem with other forms and documents. Understanding these documents can help ensure comprehensive coverage and compliance with contractual obligations. Below is a list of related documents that are frequently used alongside the Additional Insured form.

Being familiar with these documents can significantly enhance your understanding of insurance coverage and risk management. It is vital to ensure that all necessary forms are in place to protect your interests and fulfill contractual obligations effectively.

When filling out the Additional Insured form, it's important to follow certain guidelines to ensure accuracy and compliance. Here are four things you should and shouldn't do:

Understanding the Additional Insured form is crucial for businesses and contractors. However, several misconceptions can lead to confusion. Here are six common misconceptions:

Clarifying these misconceptions can help businesses better navigate their insurance needs and responsibilities.

When filling out and using the Additional Insured form, there are several important considerations to keep in mind. Below are key takeaways that can guide you through the process:

By keeping these points in mind, you can effectively navigate the complexities of the Additional Insured form and ensure that all parties are adequately protected.