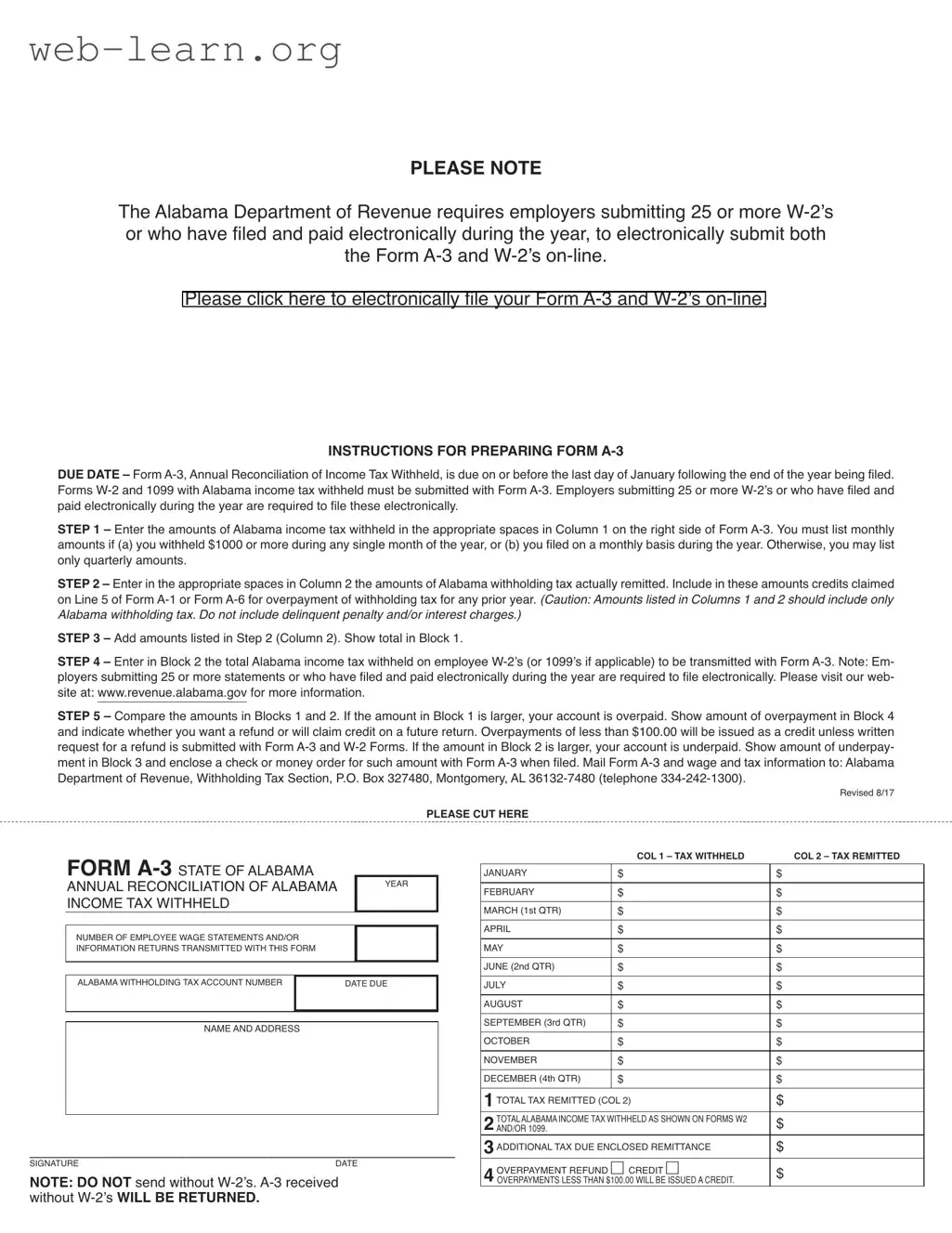

The A-3 Alabama form serves as an essential tool for employers in the state, facilitating the annual reconciliation of income tax withheld from employee wages. This form must be submitted by the last day of January following the end of the tax year, ensuring that all withholdings are accurately reported and reconciled. For employers who have withheld Alabama income tax from 25 or more W-2s, or who have filed and paid electronically during the year, electronic submission is mandatory. The form requires employers to detail the amounts of income tax withheld and the corresponding amounts actually remitted to the state, providing a clear picture of their tax obligations. Employers must carefully enter monthly amounts if they withheld $1,000 or more in any single month, while others may report quarterly totals. Additionally, the form includes sections for reporting total amounts withheld on W-2s and for addressing any discrepancies between the amounts withheld and remitted. If an employer has overpaid, they can indicate their preference for a refund or a credit toward future returns. Conversely, underpayments must be addressed promptly by including the owed amount with the submitted form. It is crucial that employers attach the necessary W-2 forms, as submissions without these documents will be returned. The A-3 form not only ensures compliance with state tax laws but also helps maintain the integrity of Alabama's tax collection system.

| Fact Name | Description |

|---|---|

| Filing Requirement | Employers submitting 25 or more W-2s must electronically file Form A-3 and W-2s. |

| Due Date | Form A-3 is due by the last day of January following the end of the tax year. |

| Submission of W-2s | Forms W-2 and 1099 with Alabama income tax withheld must be submitted with Form A-3. |

| Monthly Reporting | Employers must list monthly amounts in Column 1 if they withheld $1,000 or more in any month. |

| Overpayment Refunds | Overpayments under $100 will be credited unless a refund request is submitted with Form A-3. |

| Underpayment Process | If underpaid, the employer must show the amount in Block 3 and include payment with Form A-3. |

| Governing Law | The form is governed by Alabama state tax laws, specifically under Title 40, Chapter 18 of the Alabama Code. |

Filling out the A-3 Alabama form involves a series of steps to ensure accurate reporting of income tax withheld from employees. This form must be submitted along with W-2s and is due by the last day of January following the year being reported. Following the steps carefully will help ensure compliance with state requirements.

After completing these steps, ensure that the form is signed and dated. Do not forget to include the W-2s, as the A-3 will be returned if submitted without them. Mail the completed Form A-3 and the accompanying wage and tax information to the Alabama Department of Revenue, Withholding Tax Section, at the specified address.

What is the A-3 Alabama form?

The A-3 Alabama form is the Annual Reconciliation of Income Tax Withheld. Employers use this form to report the total amount of Alabama income tax withheld from employees' wages throughout the year. It must be filed along with W-2 and 1099 forms that show the taxes withheld.

When is the A-3 form due?

The A-3 form is due on or before the last day of January following the end of the year you are reporting. For example, if you are reporting for the year 2023, your A-3 form must be submitted by January 31, 2024.

Who needs to file the A-3 form electronically?

If you are an employer submitting 25 or more W-2s or if you have filed and paid electronically during the year, you are required to file the A-3 form electronically. This ensures a faster and more efficient processing of your tax information.

What information do I need to complete the A-3 form?

To complete the A-3 form, you will need to provide:

What should I do if my account is overpaid?

If the amount in Block 1 (total tax remitted) is larger than the amount in Block 2 (total tax withheld), your account is overpaid. You can indicate the amount of overpayment in Block 4 and choose whether you want a refund or to claim a credit on a future return.

What if my account is underpaid?

If the amount in Block 2 is larger than the amount in Block 1, your account is underpaid. You will need to show the amount of underpayment in Block 3 and include a check or money order for that amount when you file the A-3 form.

Where do I send the A-3 form?

You should mail the completed A-3 form along with the W-2 and 1099 forms to:

Alabama Department of Revenue, Withholding Tax Section,

P.O. Box 327480,

Montgomery, AL 36132-7480

If you have questions, you can call them at 334-242-1300.

What happens if I send the A-3 form without W-2s?

If you send the A-3 form without the accompanying W-2s, it will be returned to you. It is crucial to include all required documents to avoid delays in processing.

When filling out the A-3 Alabama form, individuals often make mistakes that can lead to complications in their tax filings. One common error is failing to submit the required W-2 forms alongside the A-3. The Alabama Department of Revenue explicitly states that the A-3 will be returned if W-2s are not included. This oversight can delay processing and create unnecessary confusion.

Another frequent mistake involves incorrect entries in the amounts of Alabama income tax withheld. In Column 1, employers must list monthly amounts if they withheld $1,000 or more in any single month or filed on a monthly basis. Failing to adhere to these guidelines can result in inaccurate reporting, which may lead to discrepancies in tax liability.

Many filers also neglect to include credits claimed on Line 5 of Form A-1 or Form A-6 when entering amounts in Column 2. This step is crucial, as it affects the total Alabama withholding tax actually remitted. Omitting these credits can lead to an inflated tax liability, which could have been avoided.

Additionally, errors often occur when comparing the totals in Blocks 1 and 2. If the amount in Block 1 exceeds that in Block 2, the filer must indicate the overpayment in Block 4. Conversely, if Block 2 is larger, the underpayment must be shown in Block 3. Miscalculating these amounts can lead to incorrect filings, resulting in potential penalties.

Finally, many individuals do not pay attention to the due date for submitting the A-3 form. It is due on or before the last day of January following the end of the year being filed. Missing this deadline can result in penalties and interest charges, further complicating the tax situation.

The A-3 Alabama form is a crucial document for employers in Alabama, serving as the Annual Reconciliation of Income Tax Withheld. Alongside this form, there are several other documents that employers often need to prepare or submit. Understanding these forms can help ensure compliance with state regulations and streamline the filing process.

By familiarizing themselves with these forms, employers can ensure they meet their tax obligations accurately and on time. Proper preparation and submission of the A-3 and its accompanying documents are essential for maintaining compliance with Alabama tax regulations.

The A-3 Alabama form is an important document for employers in Alabama. It serves as the Annual Reconciliation of Income Tax Withheld. Several other forms share similarities with the A-3 in terms of purpose, filing requirements, and the information they collect. Below is a list of eight documents that are similar to the A-3 Alabama form:

Understanding these forms can help ensure compliance with tax obligations and facilitate accurate reporting. Always consult with a tax professional for specific guidance related to your situation.

When completing the A-3 Alabama form, it is essential to follow specific guidelines to ensure accuracy and compliance. Here is a list of dos and don'ts to keep in mind:

Understanding the A-3 Alabama form is crucial for employers to ensure compliance and accurate reporting. However, several misconceptions can lead to confusion. Below are seven common misconceptions, along with clarifications to help you navigate the process.

By addressing these misconceptions, employers can better prepare their submissions and ensure compliance with Alabama tax regulations. For more detailed information, visiting the Alabama Department of Revenue's website is recommended.

Here are key takeaways for filling out and using the A-3 Alabama form: