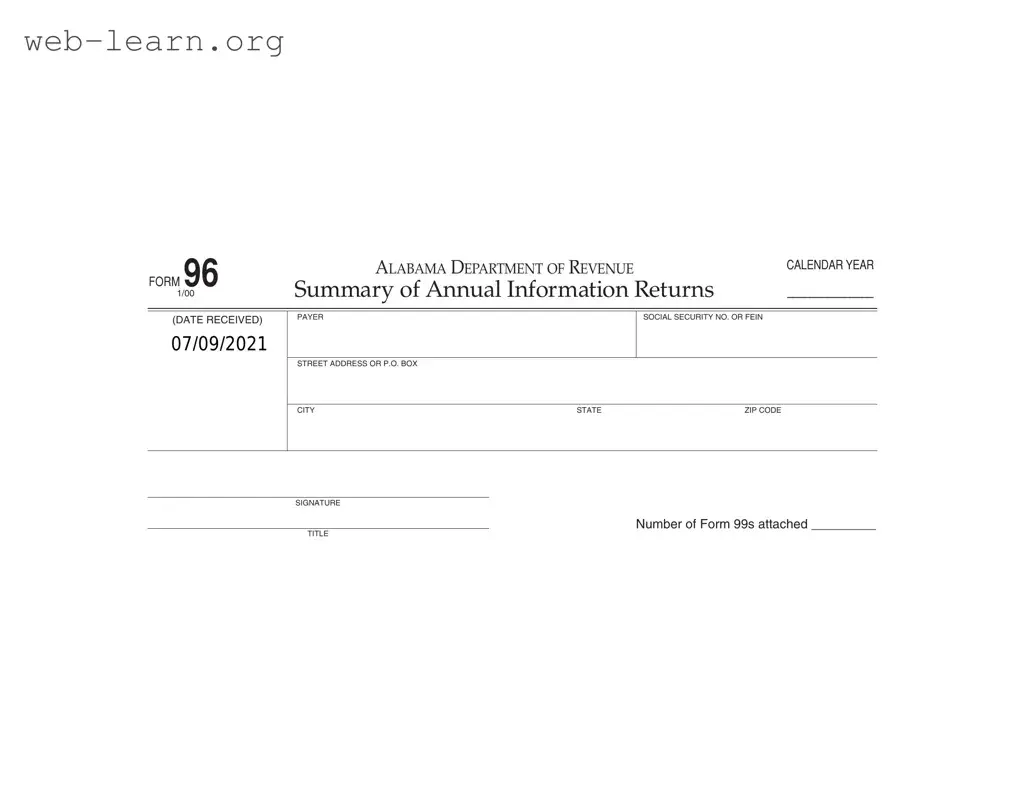

The 96 Alabama form serves as a crucial document for reporting annual information returns to the Alabama Department of Revenue. This form is designed for individuals, corporations, associations, or agents who make payments of $1,500 or more in gains, profits, or income to any taxpayer subject to Alabama income tax during a calendar year. It is essential to note that if Alabama income tax has been withheld from such payments, the filer must submit Form 99 or an approved substitute, regardless of the payment amount. Employers who have already reported salaries and wages through Form A-2 are not required to duplicate those payments on Form 99. Instead, they may opt to submit copies of federal Form 1099 to meet their reporting obligations. The deadline for filing this form is March 15 of the year following the calendar year in which the payments were made, ensuring timely compliance with state tax regulations. For any returns that include withheld Alabama income tax, it is important to use Form A-3 for annual reconciliation instead of Form 96. Proper completion and submission of this form help maintain transparency and accountability in financial dealings within the state.

| Fact Name | Details |

|---|---|

| Purpose | The 96 Alabama form is used to summarize annual information returns for payments made to taxpayers subject to Alabama income tax. |

| Filing Requirement | Every resident individual, corporation, association, or agent making payments of $1,500 or more in a calendar year must file this form. |

| Payment Type | This form covers payments made as gains, profits, or income, excluding interest coupons payable to bearer. |

| Filing Deadline | Returns must be filed by March 15 of the following year to the Alabama Department of Revenue. |

| Alternative Filing | Instead of Form 99, filers may submit copies of federal Form 1099 to fulfill reporting requirements. |

| Withholding Tax | If Alabama income tax has been withheld, Form A-3 should be used instead of Form 96. |

| Governing Law | This form is governed by Alabama state tax law, specifically regarding income tax reporting and withholding. |

Filling out the 96 Alabama form requires attention to detail and accurate information. This form is essential for reporting certain payments made to taxpayers subject to Alabama income tax. Ensure you have all necessary information at hand before you begin. Follow the steps below to complete the form correctly.

Once the form is submitted, it will be processed by the Alabama Department of Revenue. Ensure you keep a copy for your records, as you may need it for future reference or if any questions arise regarding your submission.

What is the purpose of Form 96 in Alabama?

Form 96 is used to summarize annual information returns related to payments made to individuals or entities subject to Alabama income tax. This form is specifically designed for reporting payments of $1,500 or more made during the calendar year, which could include gains, profits, or other income. It helps ensure compliance with Alabama tax laws.

Who is required to file Form 96?

Every resident individual, corporation, association, or agent making qualifying payments must file Form 96. This includes anyone making payments of $1,500 or more to a taxpayer subject to Alabama income tax. If you have withheld Alabama income tax from these payments, you must also file Form 99 or an approved substitute.

What types of payments must be reported on Form 96?

Form 96 must report payments of gains, profits, or income exceeding $1,500. However, it does not include interest coupons payable to bearer. Payments related to salaries and wages that are reported on Form A-2 do not need to be included on Form 96.

What should I do if I have withheld Alabama income tax?

If you have withheld Alabama income tax on payments reported on Form 99, do not use Form 96. Instead, you should complete Form A-3, which is the Annual Reconciliation of Alabama Income Tax Withheld. This ensures that your withholding is properly accounted for.

When is Form 96 due?

Form 96 must be filed with the Alabama Department of Revenue on or before March 15 of the year following the calendar year in which the payments were made. Timely filing is crucial to avoid penalties or issues with compliance.

How do I submit Form 96?

To submit Form 96, mail it to the Alabama Department of Revenue at the address provided in the form instructions. The address is:

Can I use copies of federal Form 1099 instead of Form 99?

Yes, in lieu of filing Form 99, you may file copies of federal Form 1099 with the Alabama Department of Revenue. This option simplifies the reporting process for those who already prepare federal forms.

What happens if I miss the filing deadline?

Missing the filing deadline can lead to penalties or interest charges imposed by the Alabama Department of Revenue. It is important to file on time to avoid these potential issues. If you realize you have missed the deadline, it is advisable to file as soon as possible to mitigate any consequences.

Filling out the 96 Alabama form can be a straightforward process, but many individuals make common mistakes that can lead to complications. One frequent error is failing to provide accurate identification numbers. The form requires a Social Security Number or Federal Employer Identification Number (FEIN), and omitting or misentering this information can delay processing.

Another common mistake is incorrect address information. The form asks for a complete street address or P.O. Box, city, state, and ZIP code. Incomplete or incorrect addresses can result in important documents being sent to the wrong location, causing further issues.

Many filers overlook the importance of signing the form. A signature is required to validate the submission. Without it, the form may be considered incomplete, leading to potential penalties or the return of the form for correction.

Some individuals fail to attach the required number of Form 99s. The form specifies the need to indicate the number of Form 99s attached. Neglecting this detail can create confusion and result in processing delays.

Another mistake involves misunderstanding the filing requirements. The form is specifically for reporting payments of $1,500 or more made to taxpayers subject to Alabama income tax. Failing to recognize this threshold can lead to unnecessary filings.

People often misinterpret the instructions regarding withholding tax. If Alabama income tax has been withheld, filers should not use Form 96 but rather Form A-3 for annual reconciliation. Ignoring this instruction can lead to complications in tax reporting.

Additionally, some individuals do not pay attention to the deadline for filing. The form must be submitted by March 15 of the following year. Missing this deadline can result in penalties and interest on any taxes owed.

Another common error is failing to keep copies of submitted forms. It is crucial to retain a copy for personal records. This practice helps in case of discrepancies or audits in the future.

Lastly, individuals sometimes do not review their forms before submission. Simple mistakes such as typos or miscalculations can lead to significant issues. A thorough review can help catch these errors before the form is sent.

By avoiding these common mistakes, individuals can ensure a smoother filing process and reduce the risk of complications with the Alabama Department of Revenue.

The 96 Alabama form is an essential document for reporting certain income payments to the Alabama Department of Revenue. However, it is often accompanied by other forms and documents that help clarify or complement the information provided. Below is a list of these related forms, each serving a specific purpose in the reporting process.

Understanding these forms and how they interact with the 96 Alabama form is vital for ensuring compliance with state tax regulations. Properly completing and submitting these documents can help avoid penalties and ensure accurate reporting of income payments.

The 96 Alabama form is similar to several other documents used for reporting income and tax information. Here are five documents that share similarities with the 96 Alabama form:

When filling out the 96 Alabama form, consider the following guidelines to ensure accuracy and compliance.

Misconceptions about the 96 Alabama form can lead to confusion and potential compliance issues. Here are nine common misconceptions along with clarifications:

Understanding these misconceptions can help ensure compliance with Alabama tax regulations and avoid potential penalties.

When filling out and using the 96 Alabama form, it's important to keep several key points in mind to ensure compliance and accuracy.

By keeping these takeaways in mind, you can navigate the process of filling out and using the 96 Alabama form more effectively.