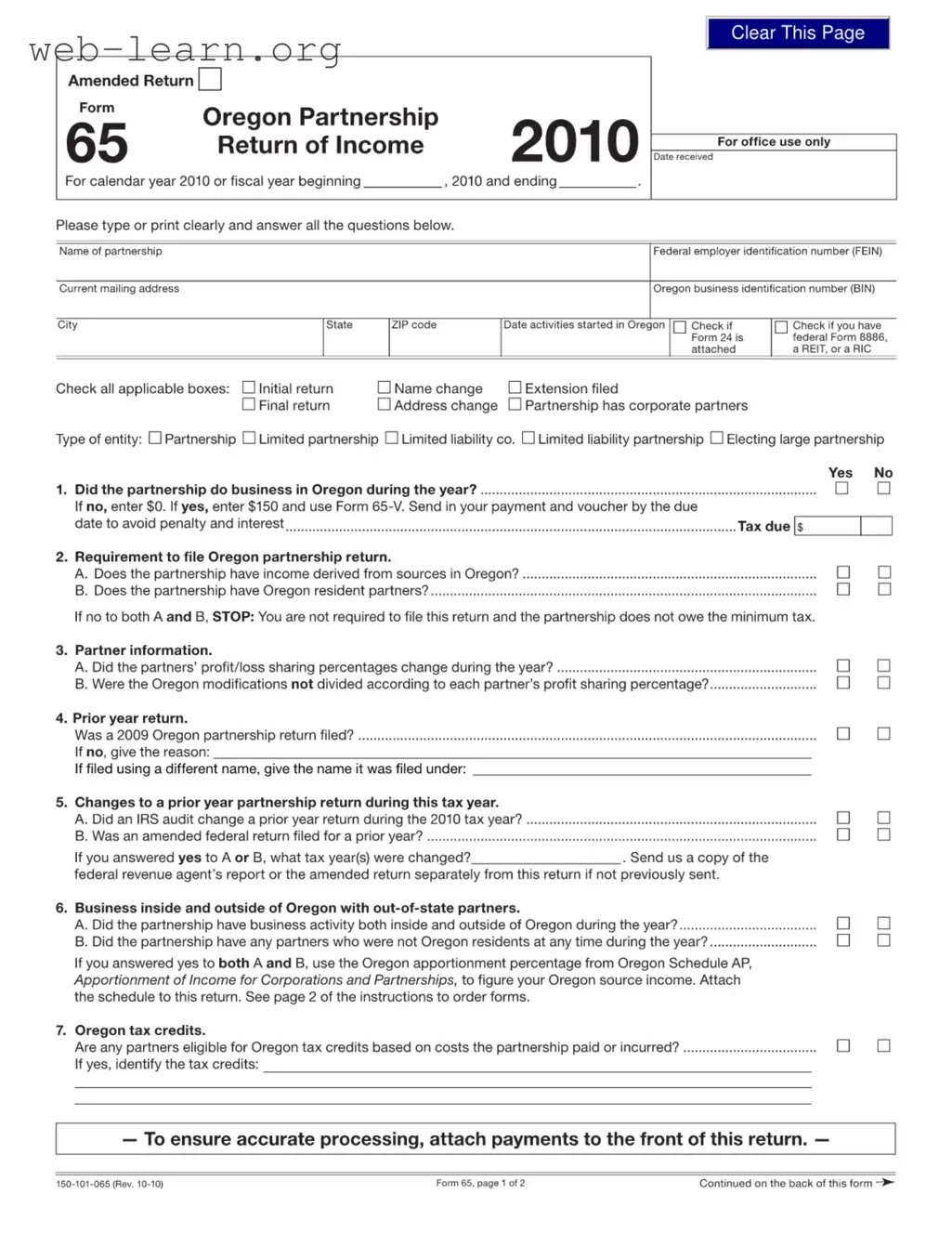

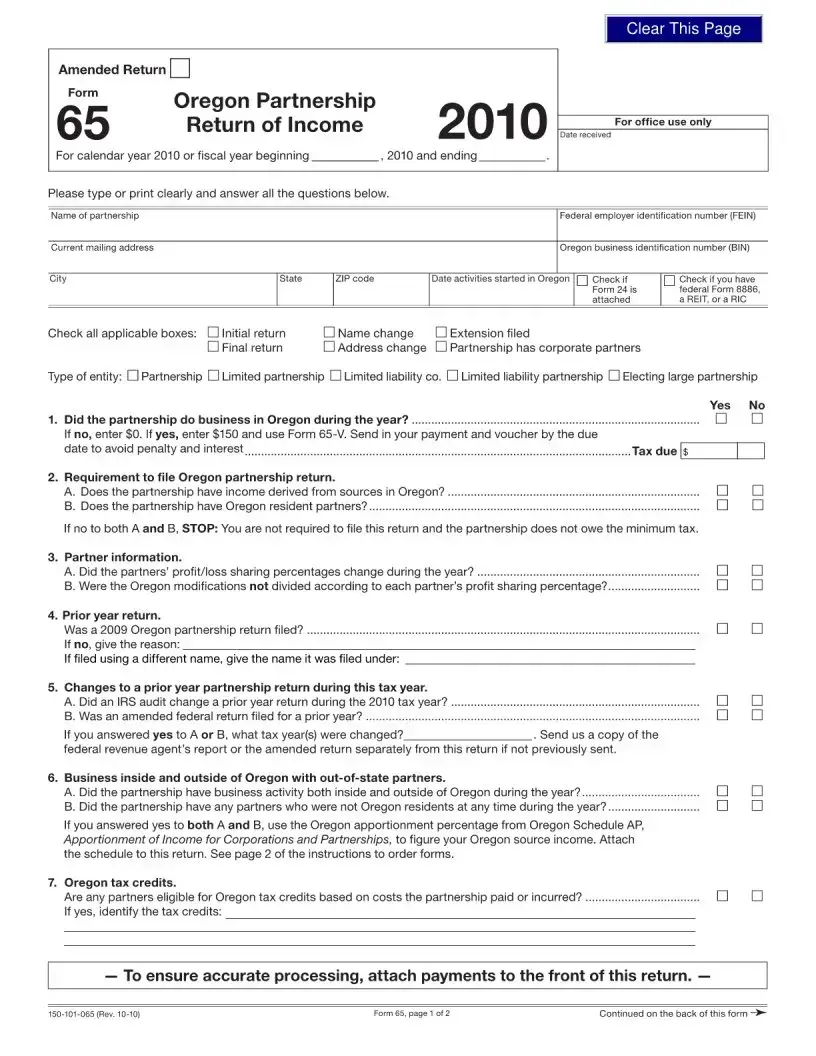

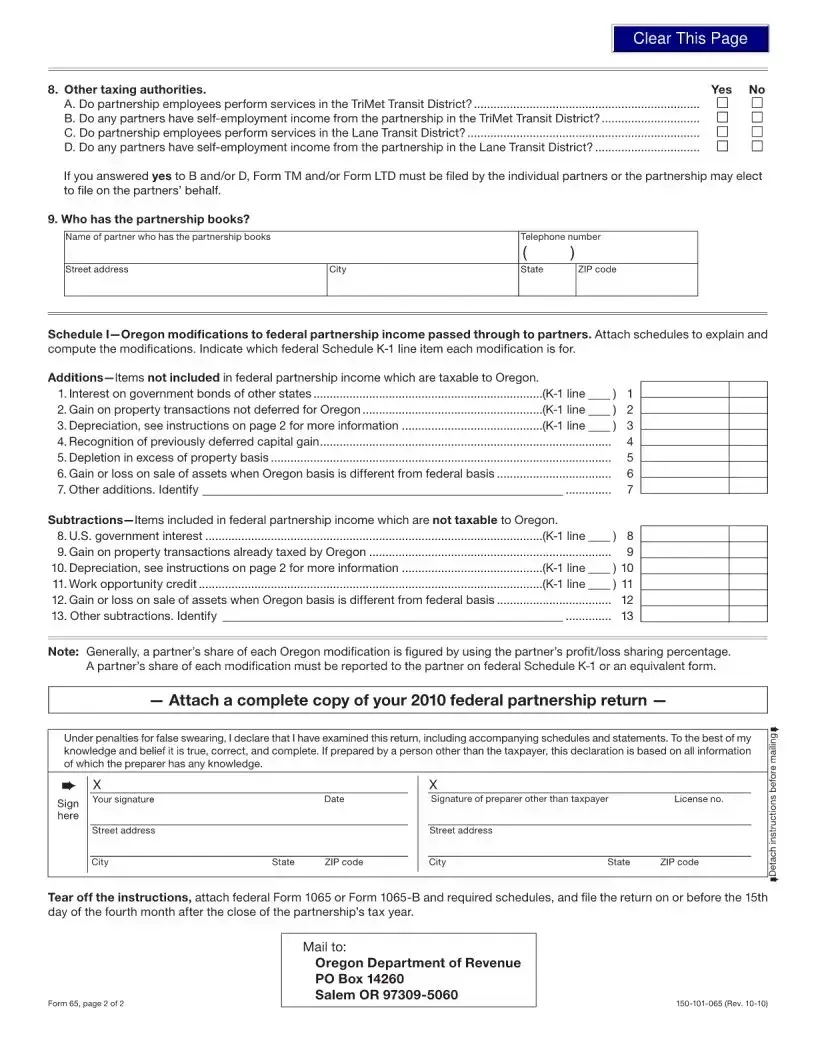

The 65 Oregon form serves as a critical document for partnerships operating within the state, outlining their income and tax obligations. Designed for partnerships that derive income from sources in Oregon or have Oregon resident partners, this form requires careful attention to detail. It encompasses various sections that address the partnership's identification, including its name, mailing address, and federal employer identification number. Additionally, it prompts the partnership to indicate whether it is filing an initial or final return, or if there have been changes in its name or address. A key aspect of the form is the determination of whether the partnership conducted business in Oregon during the year, as this influences the minimum tax owed. If the partnership had business activities both inside and outside of Oregon, it must calculate its Oregon source income using the Oregon apportionment percentage. The form also includes inquiries about any changes to profit-sharing percentages among partners, eligibility for Oregon tax credits, and the status of prior year returns. Furthermore, it requires partnerships to disclose whether they have employees or partners engaged in services within specific transit districts, which may necessitate additional filings. Overall, the 65 Oregon form is not merely a tax return; it is a comprehensive tool that ensures partnerships fulfill their tax responsibilities while providing necessary information to the state’s revenue department.

| Fact Name | Details |

|---|---|

| Form Purpose | This form is used for the Oregon Partnership Return of Income for partnerships operating in Oregon. |

| Governing Law | The form is governed by Oregon Revised Statutes (ORS) Chapter 314. |

| Minimum Tax | Partnerships must pay a minimum tax of $150 if they do business in Oregon. |

| Filing Deadline | Returns for the 2010 calendar year were due by April 18, 2011. |

| Eligibility to File | Partnerships with income from Oregon sources or with Oregon resident partners must file. |

| Changes in Profit Sharing | The form requires disclosure of any changes in partners’ profit/loss sharing percentages during the year. |

| Required Attachments | Attach a complete copy of the 2010 federal partnership return and any necessary schedules. |

Completing the 65 Oregon form requires careful attention to detail. Each section must be filled out accurately to ensure compliance with state regulations. After submitting the form, the partnership will be processed accordingly, and any necessary payments should be attached to avoid penalties.

What is Form 65?

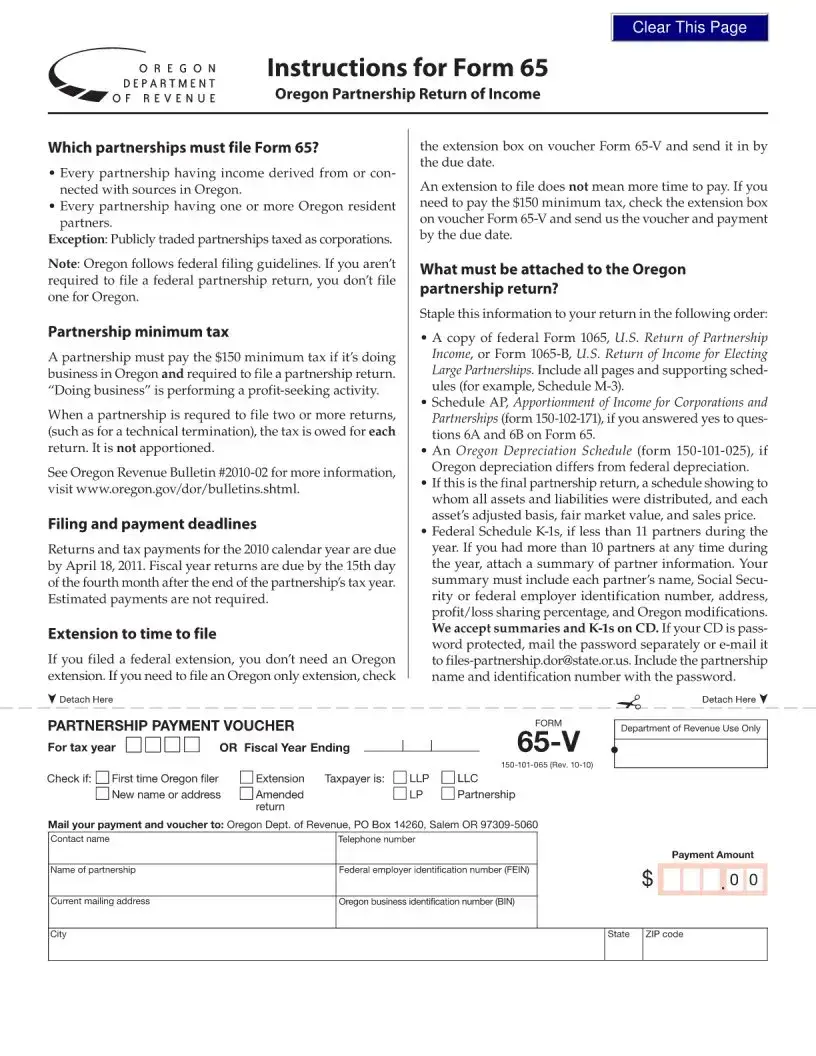

Form 65 is the Oregon Partnership Return of Income. Partnerships operating in Oregon must file this form if they have income derived from Oregon sources or if they have Oregon resident partners. The form collects information about the partnership's activities, partners, and tax obligations for the tax year.

Who is required to file Form 65?

Every partnership that either has income from Oregon sources or includes one or more Oregon resident partners must file Form 65. However, publicly traded partnerships taxed as corporations are exempt from this requirement. If a partnership is not required to file a federal return, it does not need to file for Oregon either.

What is the minimum tax for partnerships in Oregon?

Partnerships that conduct business in Oregon and are required to file a partnership return must pay a minimum tax of $150. This tax applies to each return filed, including situations where multiple returns are necessary due to technical terminations.

When are Form 65 and payments due?

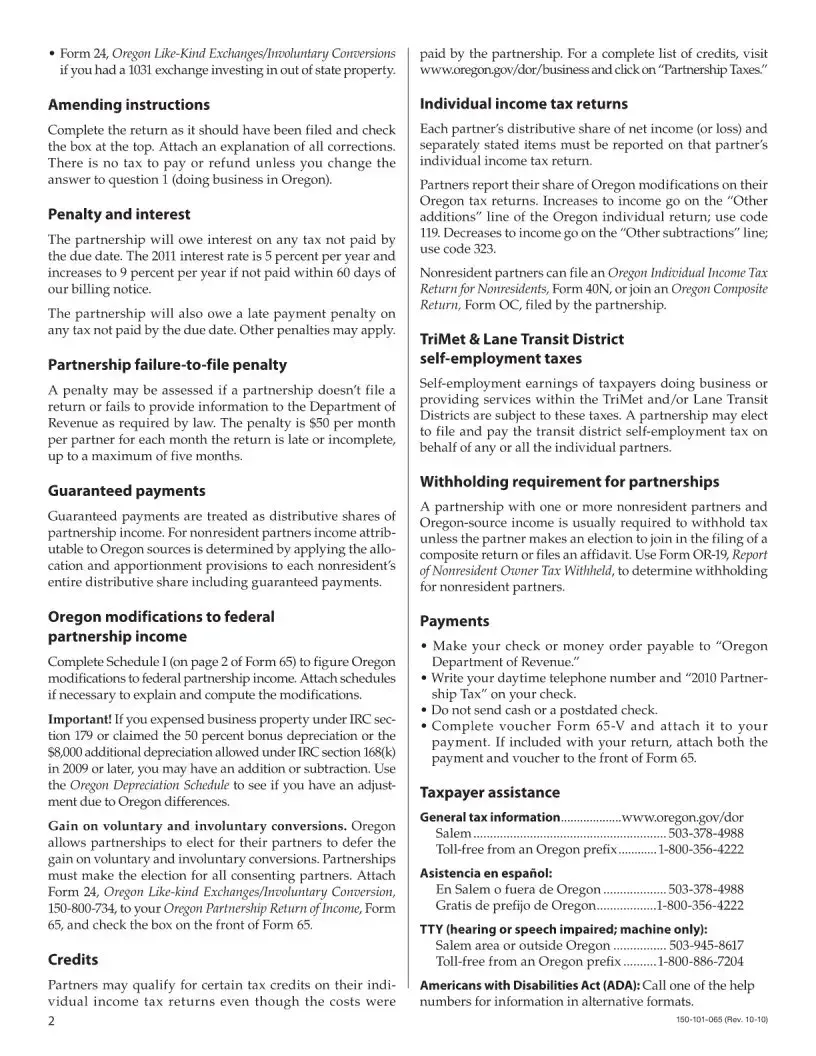

For the 2010 calendar year, Form 65 and any required tax payments were due by April 18, 2011. For partnerships with a fiscal year, the due date is the 15th day of the fourth month following the end of the tax year. Estimated payments are not required for partnerships in Oregon.

What should a partnership do if it needs an extension to file?

If a partnership has filed for a federal extension, it does not need to file a separate Oregon extension. If an Oregon-only extension is necessary, the partnership must check the extension box on Form 65-V and submit it by the due date.

What information is needed to complete Form 65?

Partnerships must provide details such as the name, mailing address, federal employer identification number (FEIN), and Oregon business identification number (BIN). Additionally, the form requires information about the partnership's business activities, changes in profit/loss sharing percentages, and any applicable tax credits.

What happens if a partnership does not have business activities in Oregon?

If a partnership did not conduct any business in Oregon during the tax year, it should enter $0 on the form. In this case, the partnership is not required to file Form 65 and does not owe the minimum tax.

Are there any specific tax credits available for partnerships in Oregon?

Yes, partnerships may qualify for Oregon tax credits based on costs incurred by the partnership. If any partners are eligible for such credits, the partnership must identify these credits on Form 65 and attach the relevant documentation.

What should a partnership do if there are changes to a prior year return?

If an IRS audit or an amended federal return has changed a prior year return, the partnership must report this on Form 65. It is essential to send a copy of the federal revenue agent's report or the amended return separately if it has not been submitted previously.

Filling out the 65 Oregon Form can be a straightforward task, but many people make common mistakes that can lead to delays or complications. One major error is failing to provide complete and accurate information about the partnership. This includes not entering the correct name, mailing address, or federal employer identification number (FEIN). Each detail is crucial for the processing of the return. Missing or incorrect information can cause the form to be rejected or delayed.

Another frequent mistake involves misunderstanding the filing requirements. Many partnerships are unsure whether they need to file based on their income sources or the residency of their partners. If a partnership does not have income from Oregon sources and no Oregon resident partners, they are not required to file the return. However, some still submit the form unnecessarily, which can lead to confusion and extra work.

Additionally, partnerships often overlook the importance of reporting changes in profit or loss sharing percentages among partners. If these percentages change during the year, it is essential to indicate this on the form. Failing to do so can result in incorrect tax calculations and complications for all partners involved.

Another common issue is related to prior year returns. Some partnerships forget to mention if they filed a return for the previous year or provide the wrong name under which it was filed. This oversight can raise questions during the review process and may require additional documentation.

Lastly, many partnerships neglect to attach necessary schedules or forms that support their claims. For example, if there are modifications to federal partnership income, those must be clearly explained and documented. Not providing these attachments can lead to processing delays or even penalties. Ensuring all required documents are included with the return is vital for a smooth filing experience.

When filing the Form 65 Oregon Partnership Return of Income, several other documents may be necessary to ensure compliance with state regulations. Each of these forms serves a specific purpose and provides additional information that may be required by the Oregon Department of Revenue. Below are four commonly used forms that accompany Form 65.

Each of these forms complements the information provided in the Form 65 and is crucial for accurate reporting and compliance with Oregon tax laws. Partnerships should carefully review their requirements to ensure all necessary documents are filed correctly and on time.

When completing the 65 Oregon form, it's important to ensure accuracy and compliance. Here’s a helpful list of things you should and shouldn't do:

Following these guidelines will help ensure a smooth filing process for your Oregon partnership return. Always double-check your work before submission to catch any errors or omissions.

There are several misconceptions regarding the 65 Oregon form that can lead to confusion for partnerships. Understanding these misconceptions can help ensure compliance and proper filing.

Filling out and using the 65 Oregon form requires careful attention to detail. Here are some key takeaways to keep in mind:

By following these guidelines, partnerships can navigate the filing process more efficiently and ensure compliance with Oregon tax regulations.