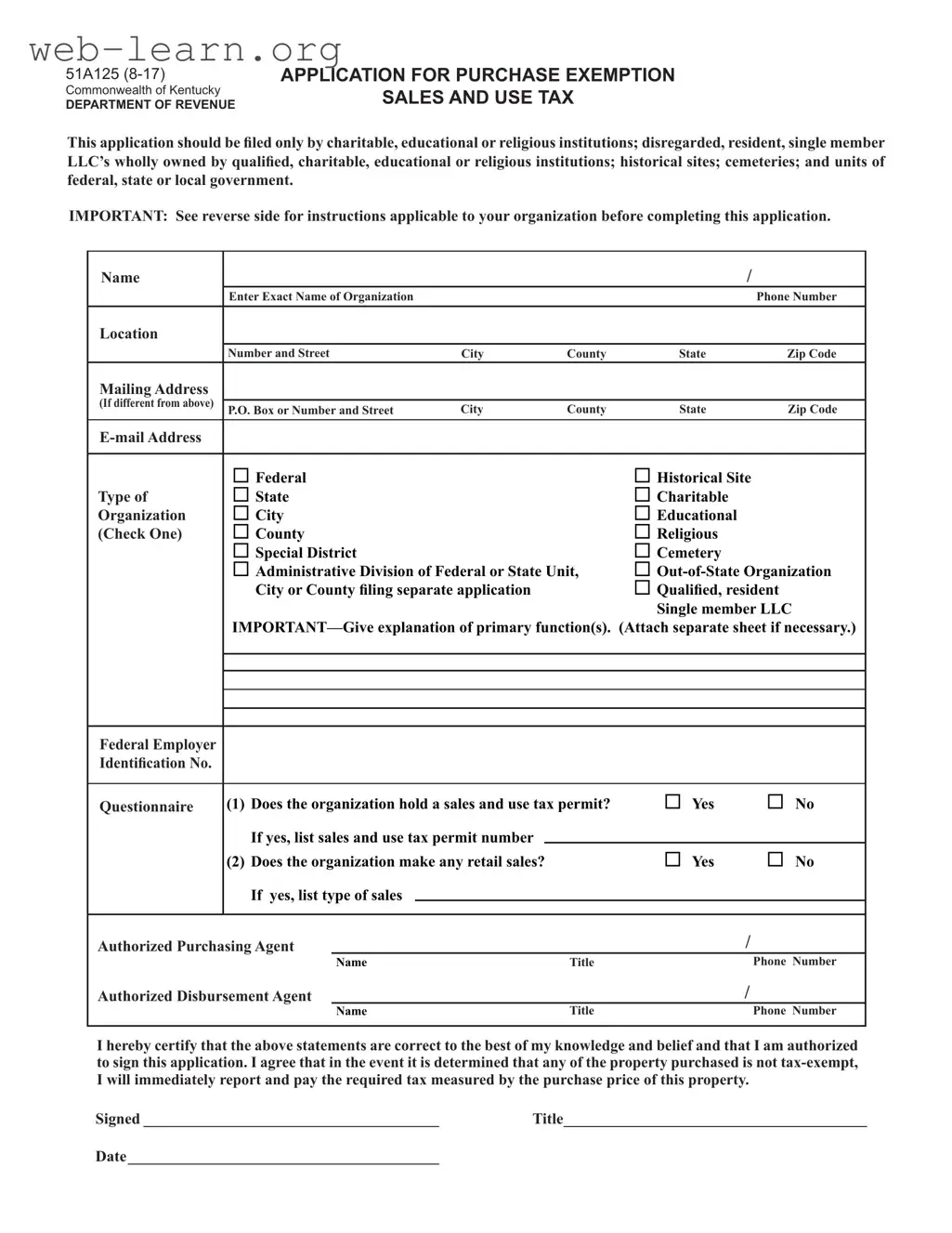

The 51A125 Kentucky form serves as an application for purchase exemption from sales and use tax, specifically designed for various organizations. Eligible applicants include charitable, educational, and religious institutions, along with historical sites, cemeteries, and certain government units. This form requires detailed information about the organization, such as its name, address, and type of entity. Additionally, it includes a questionnaire to determine the organization's sales tax permit status and whether it engages in retail sales. Supporting documents must accompany the application, such as articles of incorporation and IRS exemption letters, depending on the type of organization. Upon approval, organizations can make tax-exempt purchases related to their functions, although they must remain compliant with reporting requirements. Clear instructions are provided to ensure that applicants understand the necessary steps and documentation needed for a successful submission.

| Fact Name | Description |

|---|---|

| Purpose | The 51A125 form is an application for purchase exemption from sales and use tax, intended for specific organizations like charitable, educational, or religious institutions. |

| Eligibility | Eligible applicants include charitable organizations, educational institutions, historical sites, cemeteries, and units of government, as well as certain single-member LLCs. |

| Required Attachments | Applicants must attach relevant documents, such as Articles of Incorporation and IRS exemption letters, depending on their organization type. |

| Governing Law | This form is governed by Kentucky Revised Statutes (KRS) 65.005 and other applicable laws regarding sales and use tax exemptions. |

Filling out the 51A125 Kentucky form requires careful attention to detail. After completing the application, it will be submitted to the Kentucky Department of Revenue for processing. It is important to ensure that all required documentation is included to avoid delays in approval.

What is the purpose of the 51A125 Kentucky form?

The 51A125 form is an application for purchase exemption from sales and use tax in Kentucky. It is specifically designed for charitable, educational, and religious institutions, as well as certain other organizations like historical sites and cemeteries. By filing this form, eligible entities can obtain an exemption that allows them to purchase tangible personal property, digital property, or services without paying sales tax.

Who is eligible to file the 51A125 form?

Eligibility for the 51A125 form includes:

Each of these entities must meet specific requirements outlined in the form instructions to qualify for the exemption.

What documents are required to accompany the application?

When submitting the 51A125 form, certain documents must be attached depending on the type of organization:

What happens after the application is approved?

Upon approval of the 51A125 application, the organization will receive a letter of authorization containing an exemption number. This allows the organization to make tax-exempt purchases related to their exempt functions. However, it is important to note that any purchases made outside of these functions will still be subject to sales tax.

How should changes to the organization’s information be handled?

If there are any changes to the organization’s name, address, or nature, it is crucial to notify the Kentucky Department of Revenue promptly. Maintaining accurate information ensures that the organization can continue to benefit from its tax-exempt status without complications.

Filling out the 51A125 Kentucky form can be straightforward, but many people make common mistakes that can lead to delays or denials. One frequent error is not providing the exact name of the organization. It’s crucial to match the name exactly as it appears in official documents. Any discrepancies can raise questions and complicate the approval process.

Another mistake is failing to include the correct contact information. This includes phone numbers and email addresses. If the Department of Revenue needs to reach out for clarification, having accurate contact details is essential. Double-checking this information can save time and prevent misunderstandings.

Many applicants also overlook the requirement to attach necessary documents. For instance, charitable organizations must include a copy of their Articles of Incorporation and a letter from the IRS confirming their tax-exempt status. Failing to provide these documents will result in an incomplete application, which can lead to rejection.

Additionally, some individuals mistakenly answer the questionnaire inaccurately. For example, if the organization does hold a sales and use tax permit, this must be clearly indicated. Misleading answers can not only delay the process but may also lead to legal complications down the line.

Lastly, applicants often forget to sign and date the form. This might seem minor, but without a signature, the application is not valid. Ensure that the person authorized to sign the application does so, as this confirms the accuracy of the information provided.

The 51A125 form is essential for organizations seeking exemption from sales and use tax in Kentucky. Along with this form, several other documents may be necessary to support the application process. Each of these documents serves a specific purpose and helps ensure that the application is complete and compliant with state regulations. Below is a list of commonly used forms and documents that often accompany the 51A125 form.

Each of these documents plays a vital role in the application process for sales and use tax exemption in Kentucky. Ensuring that all necessary paperwork is accurately completed and submitted will help facilitate a smoother approval process. Proper documentation not only strengthens the application but also demonstrates the organization’s commitment to compliance with state laws.

The 51A125 Kentucky form is an application for purchase exemption from sales and use tax, specifically designed for certain organizations. Several other documents serve similar purposes in different contexts. Here are four documents that share similarities with the 51A125 form:

When filling out the 51A125 Kentucky form, it's important to follow specific guidelines to ensure a smooth application process. Here are five things you should and shouldn't do:

There are several misconceptions surrounding the 51A125 Kentucky form. Understanding these can help clarify the process for organizations seeking tax exemptions. Here is a list of nine common misconceptions:

Understanding these misconceptions can help organizations navigate the application process more effectively and ensure compliance with state regulations.