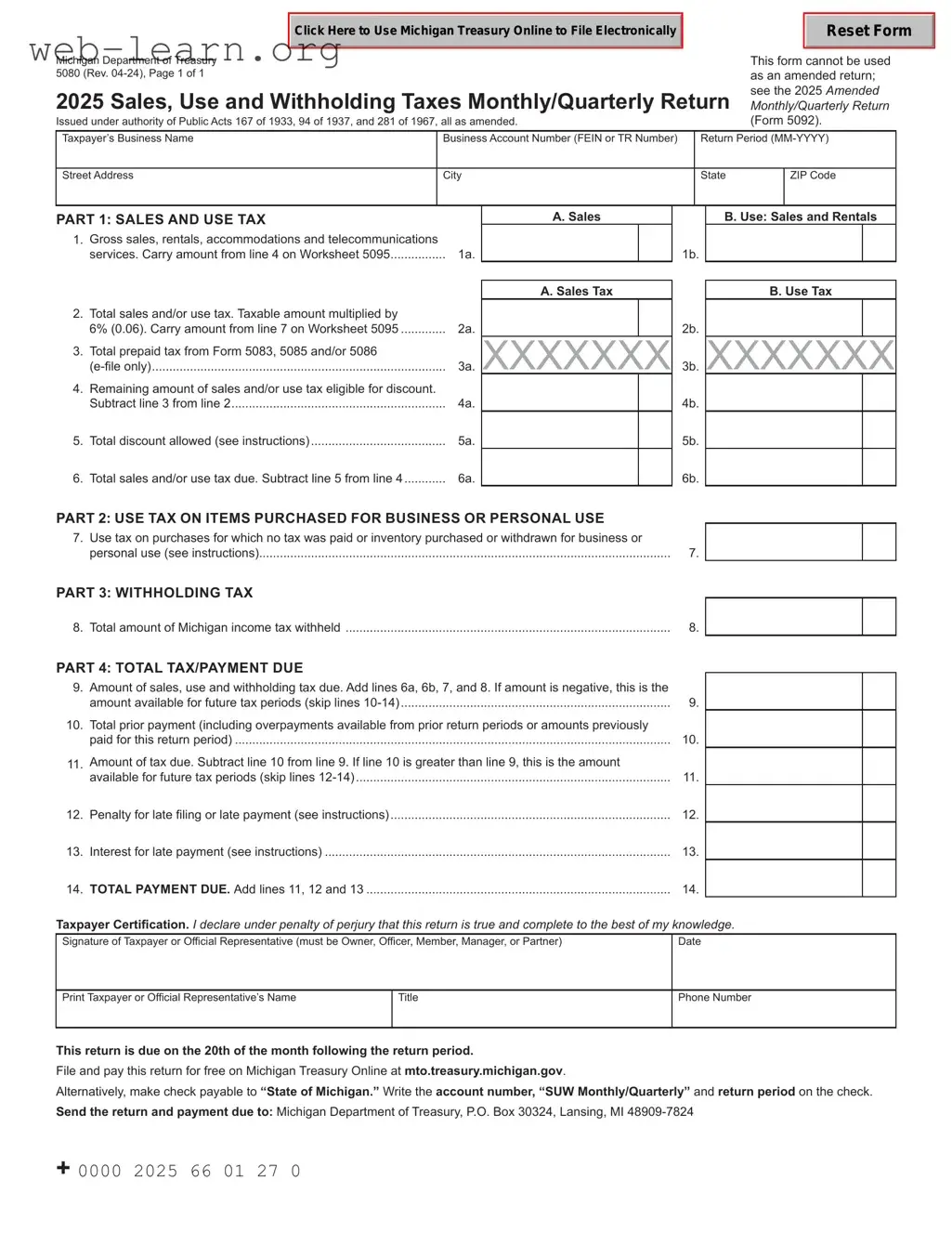

The Michigan Department of Treasury Form 5080 serves as a crucial tool for businesses in the state, enabling them to report and remit sales, use, and withholding taxes on a monthly or quarterly basis. This form is specifically designed for taxpayers to accurately declare their gross sales, rentals, and services, ensuring compliance with state tax laws. It includes several key sections, beginning with the calculation of total sales and use tax, where businesses must multiply their taxable sales by the state's 6% tax rate. Taxpayers are also required to report any pre-paid taxes from previous forms and calculate any applicable discounts based on their filing frequency. Additionally, the form addresses use tax on items purchased for business or personal use, as well as withholding tax on employee wages. The final section consolidates the total tax due, allowing taxpayers to determine any overpayments or penalties incurred due to late filings. Understanding the components of Form 5080 is essential for businesses to maintain compliance and avoid potential penalties associated with tax deficiencies.

| Fact Name | Details |

|---|---|

| Form Title | Michigan Department of Treasury 5080 (07-14) 2015 Sales, Use and Withholding Taxes Monthly/Quarterly Return |

| Governing Laws | Issued under authority of Public Acts 167 of 1933 and 94 of 1937, as amended. |

| Usage Limitation | This form cannot be used as an amended return; refer to Form 5092 for amendments. |

| Tax Types | Applicable for Sales Tax, Use Tax, and Withholding Tax. |

| Discount Eligibility | Discounts apply to 2/3 of the sales and/or use tax collected at the 6% rate. |

| Filing Frequency | Taxpayers can file monthly, quarterly, or as accelerated filers based on their tax liability. |

| Penalty for Late Filing | 5% penalty on the tax due, increasing by 5% per month, up to a maximum of 25%. |

| Interest on Late Payments | Interest is charged daily at the average prime rate plus 1 percent. |

| Payment Instructions | Make checks payable to “State of Michigan” and include your account number. |

Filling out the Michigan Department of Treasury 5080 form requires careful attention to detail. This form is essential for reporting sales, use, and withholding taxes. After completing the form, ensure that you sign it and submit it along with any payment due to the Michigan Department of Treasury.

The 5080 Michigan form is used to report sales, use, and withholding taxes to the Michigan Department of Treasury. Businesses must file this form monthly or quarterly, depending on their tax obligations. It consolidates various tax types into a single return, making it easier for taxpayers to manage their tax responsibilities.

Any business operating in Michigan that collects sales tax, use tax, or withholding tax is required to file the 5080 form. This includes retailers, service providers, and any entities that withhold income tax from employees. If a business has no tax liability for a specific period, they must still submit the form, indicating zero for the relevant lines.

To calculate the sales and use tax due, follow these steps:

If you file your return late, you will incur a penalty and interest on the amount due. The penalty starts at 5% of the tax due and increases by an additional 5% for each month or fraction thereof after the second month, capping at 25%. Interest is calculated daily based on the average prime rate plus 1%. It’s important to pay these amounts along with your tax liability to avoid further penalties.

Once you have completed the 5080 form, send it along with any payment due to the following address:

Michigan Department of Treasury

P.O. Box 30324

Lansing, MI 48909-7824

Ensure that you include your business account number on your check to facilitate proper processing.

Filling out the Michigan Department of Treasury Form 5080 can be a complex task. One common mistake is failing to report all gross sales accurately. Taxpayers often overlook including all types of sales, such as rentals or services, which can lead to an underreporting of tax liability. This error can result in significant penalties and interest if the state later determines that taxes were owed. It is crucial to ensure that every source of revenue is accounted for to avoid complications.

Another frequent mistake involves incorrectly calculating the sales and use tax due. Taxpayers sometimes misinterpret the instructions related to the multiplication of taxable sales by the applicable tax rate of 6%. Errors in calculation can lead to either overpayment or underpayment, both of which can have financial repercussions. Careful attention to detail is essential when performing these calculations to ensure compliance with tax obligations.

In addition, many individuals fail to take advantage of allowable discounts due to a lack of understanding of the discount structure. The form outlines specific criteria for discounts based on filing frequency, yet some taxpayers either do not apply the discount or miscalculate it. This oversight can result in paying more tax than necessary. Understanding the discount eligibility and calculation methods can help taxpayers minimize their tax burden.

Lastly, neglecting to sign and date the form is a common oversight. The certification section requires the taxpayer's signature, affirming that the information provided is accurate. Submitting an unsigned form can lead to delays in processing and potential penalties. It is vital to review the entire form before submission to ensure all required signatures are included, thereby avoiding unnecessary complications.

When filing the Michigan Department of Treasury 5080 form, there are several other forms and documents that may be necessary. These documents can help ensure that your tax obligations are met accurately and efficiently. Below is a list of these forms along with a brief description of each.

Using these forms in conjunction with the 5080 can help you navigate your tax responsibilities more effectively. It is important to ensure that all information is accurate and submitted on time to avoid penalties or issues with your tax filings.

Filling out the Michigan Department of Treasury 5080 form can seem daunting, but understanding the do's and don'ts can make the process smoother. Here’s a helpful list to guide you through.

By following these guidelines, you can help ensure that your submission is accurate and complete. Taking the time to understand the requirements will ultimately save you from potential issues down the road.

There are several misconceptions about the Michigan Department of Treasury 5080 form. Understanding these can help ensure accurate tax reporting and compliance.

When completing the 5080 Michigan form, understanding the details is crucial for accurate reporting and compliance. Here are key takeaways to consider:

By following these guidelines, you can ensure that your completion of the 5080 Michigan form is accurate and compliant with state regulations. This diligence can prevent potential penalties and streamline your tax reporting process.