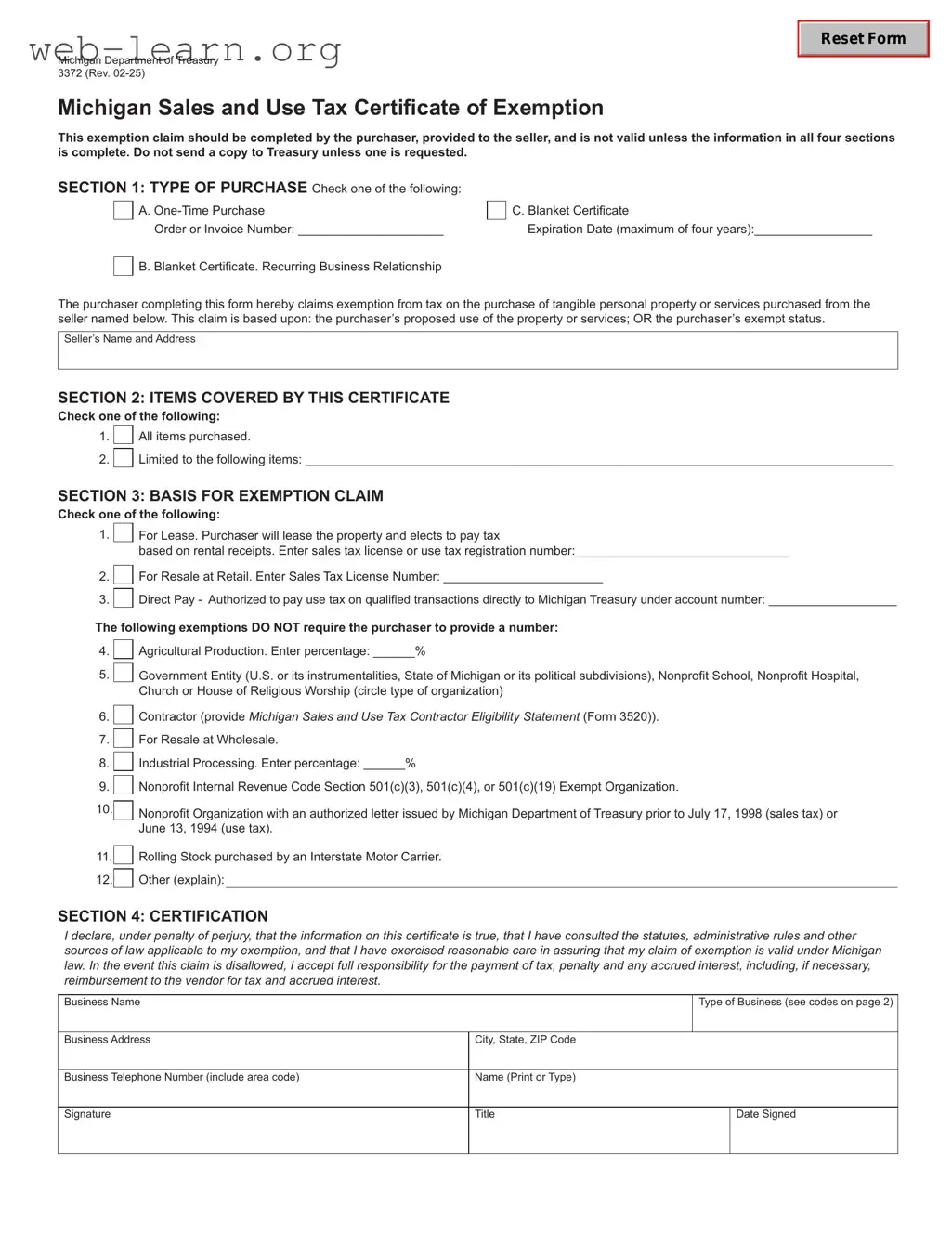

The Michigan Department of Treasury 3372 form, also known as the Michigan Sales and Use Tax Certificate of Exemption, serves an important purpose for purchasers looking to claim exemption from sales and use tax. This form must be filled out by the purchaser and provided to the seller to validate the exemption. It is crucial that all four sections of the form are completed, as an incomplete form is not valid. The first section allows the purchaser to specify the type of purchase, whether it is a one-time purchase or a blanket certificate for ongoing transactions. The second section identifies the items covered by the exemption, giving the purchaser the option to either exempt all items or specify limited items. In the third section, the purchaser must select the basis for the exemption claim, which includes various categories such as leasing, resale, and specific exemptions for agricultural production or nonprofit organizations. Finally, the fourth section requires certification from the purchaser, affirming the truthfulness of the information provided and acknowledging the responsibility for any tax liabilities if the claim is disallowed. Understanding the details of the 3372 form is essential for ensuring compliance and avoiding potential penalties.

| Fact Name | Details |

|---|---|

| Form Title | Michigan Sales and Use Tax Certificate of Exemption |

| Form Number | 3372 |

| Revision Date | Rev. 01-21 |

| Purpose | This form allows purchasers to claim exemption from Michigan sales and use tax. |

| Submission Requirement | The form must be completed and given to the seller; do not send to Treasury unless requested. |

| Sections | The form includes four sections: Type of Purchase, Items Covered, Basis for Exemption, and Certification. |

| Types of Purchase | Options include One-Time Purchase or Blanket Certificate. |

| Exemption Basis | Exemptions can be based on proposed use, exempt status, or specific categories like agricultural production. |

| Seller's Responsibility | Sellers must maintain records of exempt sales and are not allowed to rely solely on exemption numbers. |

| Governing Law | The form is governed by Michigan sales and use tax laws, as outlined in Revenue Administrative Bulletin 2016-14. |

Completing the Michigan Sales and Use Tax Certificate of Exemption (Form 3372) is an important step in claiming an exemption from sales and use tax. It is essential to provide accurate information in all sections of the form. Once completed, the form should be given to the seller and kept for your records, as it will not be submitted to the Treasury unless requested.

What is the Michigan Sales and Use Tax Certificate of Exemption (Form 3372)?

The Michigan Sales and Use Tax Certificate of Exemption (Form 3372) is a document that allows purchasers to claim exemption from sales and use tax on specific transactions. This form must be filled out by the purchaser and presented to the seller. It is essential that all sections of the form are completed for it to be valid. The form does not need to be sent to the Michigan Department of Treasury unless requested.

How do I complete the 3372 form?

Completing the form involves several key steps:

Remember, all claims are subject to audit, so ensure that your exemption is valid under Michigan law.

Who can use the 3372 form to claim an exemption?

The 3372 form can be used by various entities, including businesses, government entities, nonprofit organizations, and certain agricultural producers. If you fall into one of these categories and are purchasing tangible personal property or services that qualify for exemption, you can utilize this form. However, it’s crucial to ensure that you meet the eligibility criteria for the exemption you are claiming.

What happens if I improperly claim an exemption?

If you incorrectly claim an exemption using Form 3372, you may be held responsible for any unpaid taxes, penalties, and interest. It’s important to exercise reasonable care in understanding the exemptions available and ensuring your claim is valid. Sellers are also required to maintain proper records of exempt sales, which include keeping the exemption forms on file. Failure to comply with these requirements can lead to additional liabilities for both the purchaser and the seller.

Filling out the Michigan Department of Treasury 3372 form can be straightforward, but many people make common mistakes that can lead to complications. One frequent error occurs in Section 1, where individuals fail to select the correct type of purchase. This section requires the purchaser to indicate whether the transaction is a one-time purchase or a blanket certificate. Neglecting to check a box can invalidate the entire exemption claim.

Another mistake involves leaving out the invoice number or expiration date when applicable. For one-time purchases, the invoice number is essential. For blanket certificates, the expiration date must be included, as it cannot exceed four years. Omitting this information can result in the exemption being denied.

Section 2 often causes confusion as well. Some people check "All items purchased" without realizing that they must specify if the exemption only applies to certain items. Failing to accurately describe the items covered can lead to misunderstandings with the seller and potential tax liabilities.

In Section 3, individuals sometimes overlook the requirement to provide necessary identification numbers. Whether it is a sales tax license number or a use tax registration number, these details are crucial for verifying the exemption claim. Without them, the claim may be deemed invalid.

Another common error is related to the basis for the exemption claim. Purchasers may check the wrong box or fail to provide supporting information. It is vital to ensure that the selected exemption category accurately reflects the intended use of the purchased items or services.

Additionally, some purchasers do not take the time to read the instructions thoroughly. Each section has specific requirements that must be met for the exemption to be valid. Ignoring these guidelines can lead to incomplete submissions.

Section 4 requires a certification statement, which must be signed by the purchaser if the form is submitted in paper format. People often forget to sign or include their title, which can render the form incomplete. A missing signature can lead to the rejection of the exemption claim.

Another mistake occurs when individuals fail to consult the statutes and administrative rules relevant to their exemption claim. It is the purchaser's responsibility to ensure that their claim is valid. Ignorance of the law does not excuse improper claims, and individuals may find themselves liable for taxes, penalties, and interest.

Lastly, some purchasers mistakenly believe that the exemption certificate does not require any follow-up. In reality, all claims are subject to audit. Maintaining proper records of exempt sales, including the completed form, is essential for compliance. Failure to do so can lead to additional complications down the line.

The Michigan Department of Treasury Form 3372 is used to claim exemption from sales and use tax for specific purchases. In addition to this form, several other documents may be necessary to support or clarify the exemption claim. Below is a list of related forms and documents commonly utilized alongside Form 3372.

Each of these documents plays a crucial role in substantiating claims for tax exemption in Michigan. Proper completion and submission of these forms can help ensure compliance and avoid potential tax liabilities.

When filling out the Michigan Department of Treasury 3372 form, follow these guidelines to ensure accuracy and compliance.

Misconceptions about the Michigan Department of Treasury 3372 form can lead to confusion regarding its proper use. Here are six common misconceptions:

The Michigan Sales and Use Tax Certificate of Exemption, known as Form 3372, is a crucial document for purchasers seeking to claim exemption from sales tax on qualified transactions. Here are some key takeaways to consider when filling out and using this form:

Understanding these key points can help ensure that the exemption process is handled correctly, minimizing the risk of future complications. It is important for both purchasers and sellers to be diligent and informed when using Form 3372.