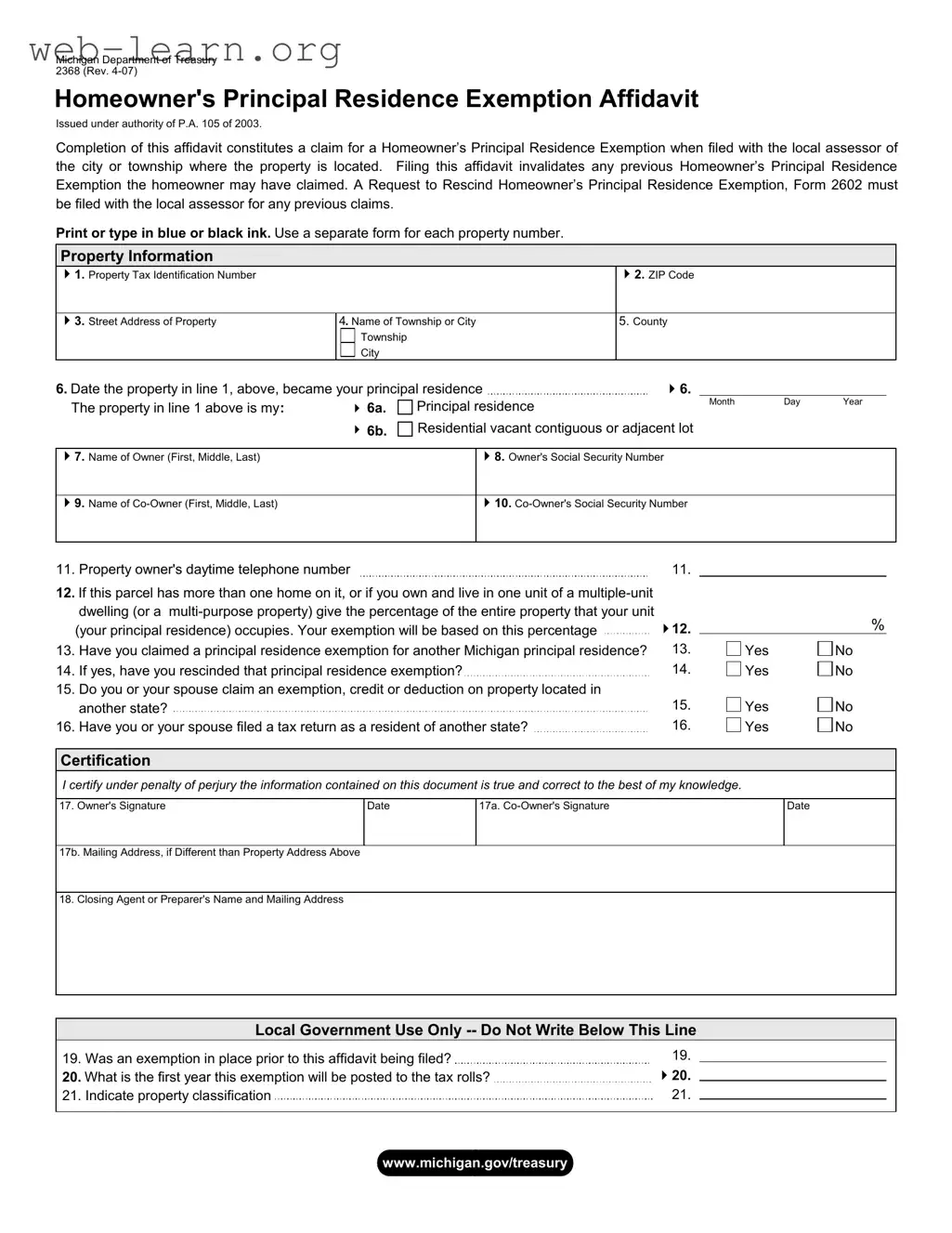

The Michigan Department of Treasury Form 2368, known as the Homeowner's Principal Residence Exemption Affidavit, plays a crucial role for homeowners seeking tax relief. This form must be filed with the local assessor in the city or township where the property is located. By submitting this affidavit, homeowners claim an exemption from a portion of local school operating taxes, providing significant financial relief. It's important to note that filing this form will invalidate any previous exemptions the homeowner may have claimed. Each property requires a separate form, and the affidavit must be completed in blue or black ink. Key information includes the property tax identification number, the owner’s details, and the date the property became the principal residence. Homeowners must also disclose if they have claimed an exemption for another property or if they have filed a tax return as a resident in another state. The form includes a certification section where homeowners affirm the accuracy of their information under penalty of perjury. For those with multiple residences, specific calculations determine the percentage of the property that qualifies for the exemption. Understanding these requirements is essential for homeowners to navigate the tax exemption process effectively.

| Fact Name | Description |

|---|---|

| Form Purpose | The Michigan Department of Treasury 2368 form is used to claim a Homeowner's Principal Residence Exemption. This exemption can reduce a portion of local school operating taxes for homeowners who occupy their principal residence. |

| Governing Law | This form is issued under the authority of Public Act 105 of 2003, which governs the eligibility and process for claiming the exemption. |

| Filing Deadline | Homeowners must file this affidavit with their local assessor by May 1st of the year they wish to claim the exemption. Timely submission is crucial for receiving the tax benefits. |

| Impact of Filing | Filing this form invalidates any previous Homeowner’s Principal Residence Exemption claims. Homeowners must ensure they have rescinded any prior exemptions by using Form 2602. |

| Owner's Certification | By signing the form, homeowners certify that the information provided is true and correct. This certification is under penalty of perjury, emphasizing the importance of accuracy in the claims made. |

Filling out the Michigan Department of Treasury Form 2368 is an important step for homeowners seeking a principal residence exemption. This form needs to be completed carefully and submitted to the local assessor by May 1st of the claim year. Ensure all information is accurate to avoid any issues with your exemption claim.

The Michigan Form 2368, also known as the Homeowner's Principal Residence Exemption Affidavit, is used to claim an exemption from a portion of local school operating taxes for your principal residence. When filed with your local assessor, this form helps reduce your property tax burden if you occupy the property as your primary home.

This form should be completed by homeowners who occupy their property as their principal residence. It is important to note that renters should not file this form, as it is specifically designed for property owners.

The form requires various details, including:

Accurate information is crucial for your exemption claim to be processed correctly.

If you have claimed a principal residence exemption before, filing the Form 2368 will invalidate that previous exemption. To rescind the prior exemption, you must file Form 2602 with your local assessor.

Filing the Form 2368 can result in a reduction of your local school operating taxes on your property. However, it does not affect the overall assessment value of your property. Your local assessor will adjust your taxes on your next property tax bill once the form is processed.

If you stop using the property as your principal residence, you must notify your local assessor within 90 days of the change. Failure to do so may result in penalties. This notification can be made using Form 2602, which is the Request to Rescind Homeowner's Principal Residence Exemption.

The completed Form 2368 must be filed with your township or city assessor by May 1st of the year in which you are claiming the exemption. Timely submission is essential to ensure your exemption is applied to your property tax bill for that year.

After completing the form, mail it to the township or city assessor where the property is located. The appropriate address can usually be found on your most recent tax bill or assessment notice. Do not send the form directly to the Michigan Department of Treasury.

Filling out the Michigan Department of Treasury Form 2368 can be a straightforward process, but many individuals make common mistakes that can lead to delays or complications in receiving their Homeowner’s Principal Residence Exemption. Understanding these pitfalls can help ensure a smoother application experience.

One frequent error is failing to include the Property Tax Identification Number. This number is essential for identifying the property in question. Without it, the local assessor cannot process the exemption correctly. Always double-check your tax bill or assessment notice to ensure you have the correct number.

Another mistake involves not using the correct ink color. The instructions specify that applicants should print or type in blue or black ink. Using any other color can lead to confusion and may result in the form being rejected. Consistency in presentation is key to clarity.

Many applicants also neglect to indicate the correct date when the property became their principal residence. This date is crucial for determining eligibility. Providing an inaccurate date can complicate the assessment process and may lead to a denial of the exemption.

In addition, some people mistakenly believe that they can claim multiple principal residences. However, the rules stipulate that you may only have one principal residence at a time. Misunderstanding this can lead to issues, particularly if you have claimed exemptions for properties in different locations.

Another common oversight is not providing the required Social Security Numbers for all owners. This information is necessary for verification purposes. Omitting this detail can raise red flags and slow down the processing of the application.

Additionally, applicants often forget to sign and date the form. Certification is a critical step that confirms the accuracy of the information provided. A missing signature can result in the form being deemed incomplete and lead to further delays.

When it comes to multiple-unit properties, individuals sometimes fail to calculate the correct percentage of the property that constitutes their principal residence. This calculation is essential for determining the exemption amount. If you own a duplex, for example, accurately measuring the living space is vital to avoid complications.

Some applicants also overlook the requirement to file a Request to Rescind if they have previously claimed an exemption on another property. Not doing so can lead to penalties and disqualification from receiving the current exemption.

Lastly, many individuals do not pay attention to the mailing instructions. It is crucial to send the completed form to the correct local assessor, not directly to the Department of Treasury. Misaddressing the form can result in it not being processed in a timely manner.

By being aware of these common mistakes, individuals can improve their chances of successfully obtaining the Homeowner’s Principal Residence Exemption. A careful review of the form and adherence to the guidelines can make all the difference in the application process.

When navigating the process of claiming a Homeowner's Principal Residence Exemption in Michigan, it's essential to understand the supporting documents that may be required alongside the Michigan Department of Treasury Form 2368. Each of these documents plays a vital role in ensuring that your exemption claim is processed smoothly and accurately. Below are some key forms that often accompany the 2368 form.

Understanding these documents can significantly enhance your experience with the exemption process. By ensuring that you have all the necessary forms completed and submitted, you can avoid potential delays and complications. Always consult with your local assessor if you have questions about your specific situation or the forms required.

The Michigan Department of Treasury Form 2368 is a specific document related to claiming a Homeowner's Principal Residence Exemption. Several other forms serve similar purposes in the realm of property tax exemptions and claims. Below is a list of documents that share similarities with Form 2368:

Each of these forms serves a unique purpose but shares the common goal of providing tax relief or exemption based on specific criteria and circumstances.

Do's

Don'ts

Understanding the Michigan Department of Treasury Form 2368 can be challenging due to various misconceptions. Here are five common misunderstandings about this form:

While completing the Form 2368 is necessary to apply for a Homeowner's Principal Residence Exemption, it does not automatically guarantee that you will receive the exemption. Your local assessor must review and approve your application based on eligibility criteria.

This form is specifically for homeowners who occupy their principal residence. Renters do not qualify and should not file the Form 2368.

Homeowners may only claim one principal residence at a time. If you have multiple properties, you must designate which one is your principal residence for tax exemption purposes.

If you previously claimed a Homeowner's Principal Residence Exemption and are now filing for a different property, you must rescind the previous exemption. This is done by submitting Form 2602 to your local assessor.

The exemption provided by the Form 2368 only reduces the amount of local school operating taxes. It does not impact the overall assessed value of your property.

Filling out the Michigan Department of Treasury Form 2368 is an important step for homeowners seeking a Principal Residence Exemption. Here are some key takeaways to help you navigate this process effectively:

By keeping these points in mind, you can ensure a smoother experience when filing for your Principal Residence Exemption in Michigan.