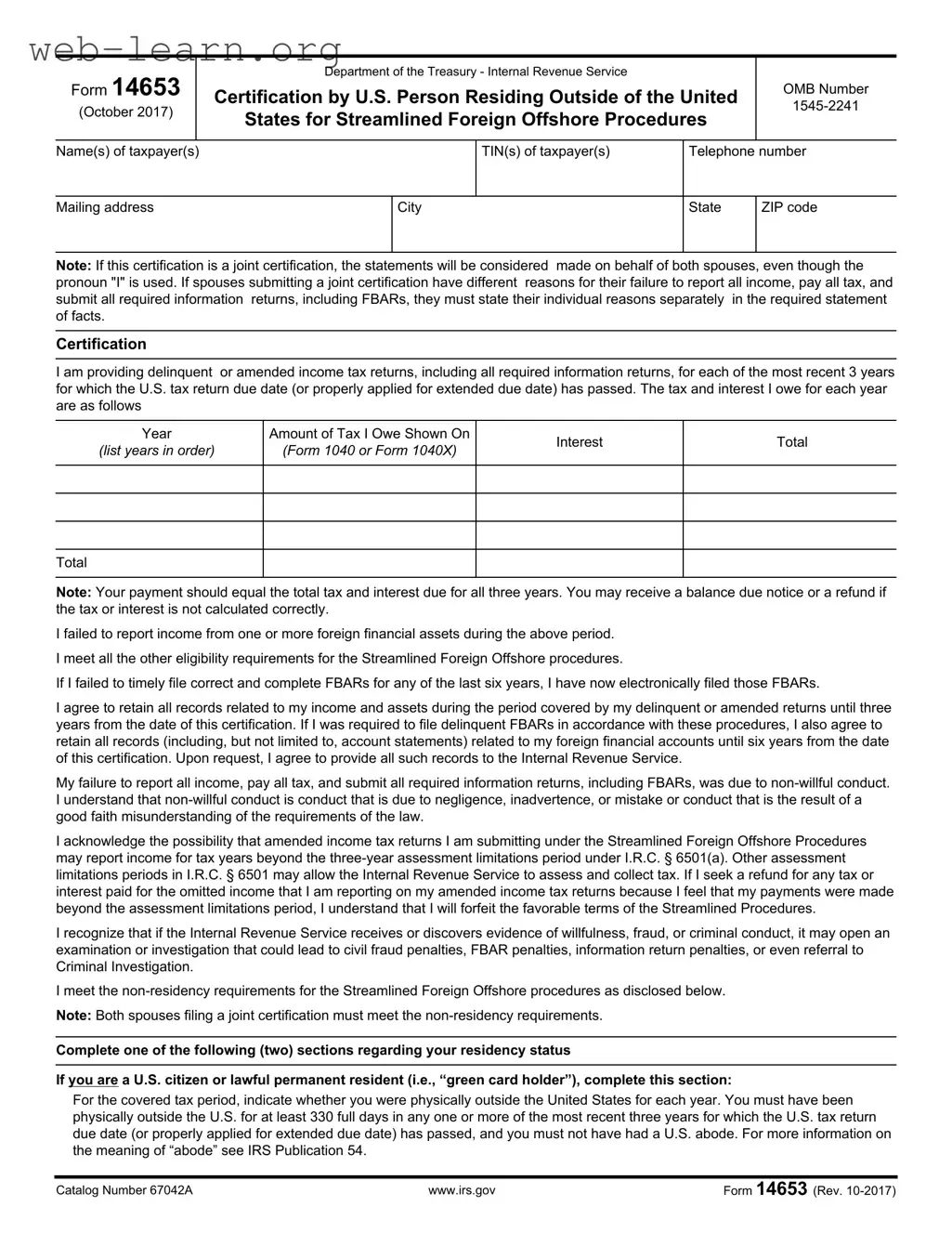

The 14653 form, officially titled "Certification by U.S. Person Residing Outside of the United States for Streamlined Foreign Offshore Procedures," plays a crucial role for U.S. taxpayers living abroad who need to rectify their tax reporting. This form, issued by the Internal Revenue Service (IRS), allows eligible individuals to certify their compliance with U.S. tax laws while seeking to benefit from streamlined procedures designed to reduce penalties. Key aspects of the form include the requirement for taxpayers to submit delinquent or amended income tax returns for the past three years, along with any necessary information returns, such as Foreign Bank Account Reports (FBARs). Taxpayers must also provide detailed narratives explaining their reasons for failing to report income and must demonstrate that their actions were non-willful, meaning they were not intentional but rather due to negligence or misunderstanding. Additionally, the form requires individuals to confirm their residency status, ensuring they meet the non-residency criteria essential for the streamlined process. Overall, the 14653 form serves as a pathway for taxpayers to come into compliance with U.S. tax obligations while minimizing the potential for severe penalties.

| Fact Name | Description |

|---|---|

| Form Purpose | Form 14653 is used by U.S. persons residing outside the United States to certify their eligibility for the Streamlined Foreign Offshore Procedures. |

| Governing Law | The form operates under the Internal Revenue Code (IRC) sections related to tax compliance and reporting. |

| Eligibility Requirements | Taxpayers must meet specific criteria, including providing delinquent or amended returns for the last three years. |

| Non-Willful Conduct | Taxpayers must declare that their failure to report income was due to non-willful conduct, such as negligence or misunderstanding. |

| FBAR Compliance | If applicable, taxpayers must have electronically filed their Foreign Bank Account Reports (FBARs) for the last six years. |

| Record Retention | Taxpayers must retain records related to their income and assets for three years, and for FBARs, six years. |

| Joint Certification | Spouses can file jointly, but both must meet the non-residency requirements and state their reasons separately if they differ. |

| Assessment Limitations | Taxpayers acknowledge the possibility of reporting income beyond the three-year assessment period under IRC § 6501(a). |

| Consequences of Willfulness | If the IRS finds evidence of willful conduct, it may lead to civil or criminal penalties. |

| Submission Completeness | Failure to provide a narrative statement of facts will result in an incomplete submission, disqualifying the taxpayer from relief. |

Filling out Form 14653 is a crucial step for U.S. persons living abroad who wish to participate in the Streamlined Foreign Offshore Procedures. This form requires careful attention to detail, as it involves providing personal information, tax details, and an explanation of any previous reporting failures. Here’s how to proceed with filling out the form effectively.

After completing the form, review it carefully to ensure all information is accurate and complete. Submit the form along with any required attachments to the IRS. This step is essential to ensure compliance and avoid potential penalties.

Form 14653 is a certification used by U.S. persons residing outside of the United States who wish to participate in the Streamlined Foreign Offshore Procedures. This form allows individuals to certify their compliance with U.S. tax laws, particularly when they have failed to report income, pay taxes, or submit required information returns, including FBARs (Foreign Bank Account Reports). By submitting this form, taxpayers can potentially avoid penalties associated with non-compliance.

This form is specifically designed for U.S. citizens and lawful permanent residents (green card holders) living abroad. It is applicable to those who have not reported all income from foreign financial assets and who meet the eligibility requirements for the Streamlined Foreign Offshore Procedures. Additionally, both spouses must meet the non-residency requirements if they are filing a joint certification.

To complete Form 14653, individuals must:

Providing a complete narrative statement is crucial for the acceptance of Form 14653. If the statement is incomplete or missing, the submission will be considered invalid, and the taxpayer will not qualify for the streamlined penalty relief. The narrative should include specific reasons for the failure to report income, as well as any relevant personal and financial background information.

If the IRS finds evidence of willfulness, fraud, or criminal conduct, it may initiate an examination or investigation. This could lead to severe penalties, including civil fraud penalties, FBAR penalties, or even criminal charges. It is essential for taxpayers to demonstrate that their failure to report was non-willful, meaning it resulted from negligence, inadvertence, or a misunderstanding of the law.

Filling out Form 14653 can be daunting, and mistakes can lead to delays or complications. One common error is failing to provide accurate taxpayer identification numbers (TINs). Ensure that all TINs listed are correct, as errors can cause processing issues.

Another frequent mistake involves incomplete narratives regarding the failure to report income. It's crucial to include specific details about why income was not reported, as well as any relevant personal or financial background. A vague explanation may result in the form being deemed incomplete.

Some individuals neglect to confirm their residency status accurately. If you are a U.S. citizen or a lawful permanent resident, you must indicate whether you were physically outside the United States for at least 330 full days in the relevant years. Misrepresenting this information can jeopardize your eligibility for streamlined procedures.

Additionally, many people forget to attach required documents, such as computations for those not meeting the substantial presence test. Without these attachments, the submission may be considered incomplete, which can delay the process significantly.

Another common oversight is not retaining records as stipulated. You must agree to keep all records related to your income and assets for the required periods. Failing to do so could lead to complications if the IRS requests documentation later.

Some filers also mistakenly assume that joint certifications mean they can provide a single narrative. Each spouse must include individual reasons for their failure to report income if their circumstances differ. This detail is essential for a complete submission.

Finally, individuals sometimes overlook the importance of signatures and dates. Ensure that all required signatures are present and that dates are accurate. Missing signatures can lead to the rejection of the form, causing further delays in resolution.

The Form 14653 is an important document for U.S. persons residing outside the United States seeking to participate in the Streamlined Foreign Offshore Procedures. Along with this form, several other documents may be required to ensure compliance and facilitate the process. Below is a list of these documents, along with brief descriptions of their purposes.

Each of these documents plays a crucial role in the Streamlined Foreign Offshore Procedures. Proper completion and submission of these forms can help taxpayers resolve their tax issues while minimizing penalties. It is essential to ensure that all required documents are accurate and submitted in a timely manner to facilitate the process.

The Form 14653 is an important document for U.S. persons residing outside the United States who need to certify their eligibility for the Streamlined Foreign Offshore Procedures. Several other forms serve similar purposes in addressing tax compliance and reporting requirements. Here are seven documents that share similarities with Form 14653:

Each of these forms plays a role in ensuring compliance with U.S. tax laws, particularly in relation to foreign income and assets. Understanding their similarities can help in navigating the complexities of tax reporting for U.S. citizens living abroad.

When filling out Form 14653, it's essential to approach the process with care and attention. Below is a list of important dos and don’ts to help ensure your submission is complete and accurate.

Understanding the 14653 form is crucial for U.S. taxpayers residing outside the country who are seeking to correct past tax reporting issues. Unfortunately, several misconceptions can lead to confusion and mistakes. Here are four common misconceptions about the 14653 form:

This is incorrect. Taxpayers must include a narrative statement explaining their failure to report income, pay taxes, and submit required information returns. A lack of detail can result in an incomplete submission, jeopardizing eligibility for streamlined procedures.

In reality, both spouses must meet the non-residency requirement. If the number of days each spouse was outside the U.S. differs, this must be disclosed in the form or an attachment.

This is misleading. While the streamlined procedures offer potential relief, if the IRS uncovers evidence of willfulness or fraud, penalties may still be imposed. It is essential to approach the process with transparency and honesty.

This is false. Taxpayers must retain records related to their foreign financial accounts for specified periods. Failure to do so can lead to complications or penalties if the IRS requests documentation.

Being aware of these misconceptions can help ensure a smoother process when filing the 14653 form. Take the time to understand the requirements fully, as doing so can save you from unnecessary stress and potential penalties.

When filling out Form 14653, there are several important points to keep in mind. This form is designed for U.S. persons residing outside the United States who wish to participate in the Streamlined Foreign Offshore Procedures.

Completing Form 14653 accurately and thoroughly is essential for a successful submission. Take your time to ensure that all information is correct, as incomplete submissions may not qualify for the streamlined penalty relief.